The Central Bank claims that in the past year, 2.7 million people treated insurers for reimbursement on OSAGO policies. But to seek the payment does not mean to get money; Last year, 3.4% of "Osagovts" received refusals.

Experts of RBC amounted to rating insurance companies OSAGO 2016 Based on the statistics of the Central Bank of the Russian Federation for 2015, which includes settled cases and refuses to compensive, as well as the average level of payments. According to the representative of the "headstore", this rating can be used as a manual when choosing an insurance company.

See also:

10. "Rosgosstrakh"

The largest Russian company in terms of the collected insurance premium. He has 3.5% of the OSAO bounce and on average pays to motorists 53,595 rubles for insured events, while the average market price is 47.9 thousand rubles.

9. Ingosstrakh

This company includes the top ten largest Insurers of Russia, only 3.3% of refusals for OSAGO policies. The average payment is 40,458 rubles, it does not "reach" to the average market price by 7.5 thousand rubles.

This company includes the top ten largest Insurers of Russia, only 3.3% of refusals for OSAGO policies. The average payment is 40,458 rubles, it does not "reach" to the average market price by 7.5 thousand rubles.

8. "Transneft"

It was founded in 1996 and is the "daughter" of oil-producing "transneft". In 2013, this SKA acquired Sogaz. Since 2011, the highest rating of the reliability "A ++" from the Expert RA Agency has invariably deserves. The level of failures on the CTP - 2.4%. On average, 17,511 rubles pays, it is smaller than the average market price by 30.3 thousand rubles.

It was founded in 1996 and is the "daughter" of oil-producing "transneft". In 2013, this SKA acquired Sogaz. Since 2011, the highest rating of the reliability "A ++" from the Expert RA Agency has invariably deserves. The level of failures on the CTP - 2.4%. On average, 17,511 rubles pays, it is smaller than the average market price by 30.3 thousand rubles.

7. "Uralsib"

It is one of the leading financial holdings on the Russian market. It has a high reliability rating "A +" and a low level of refusal of the CCAMA - 1.9%. The average amount reimbursed by insurance is 50,954 rubles (three thousand rubles exceeds the average market).

It is one of the leading financial holdings on the Russian market. It has a high reliability rating "A +" and a low level of refusal of the CCAMA - 1.9%. The average amount reimbursed by insurance is 50,954 rubles (three thousand rubles exceeds the average market).

6. Energogarant

Agency "Expert RA" assigned the company "Energogarant" The highest rating of reliability - "a ++" and the forecast for this rating is stable. The attractiveness of the company for car owners adds a low refusal of OSAGO payments, it keeps at 1.5%. The average amount of compensation is 45,582 rubles, only 2.4 thousand rubles less average.

Agency "Expert RA" assigned the company "Energogarant" The highest rating of reliability - "a ++" and the forecast for this rating is stable. The attractiveness of the company for car owners adds a low refusal of OSAGO payments, it keeps at 1.5%. The average amount of compensation is 45,582 rubles, only 2.4 thousand rubles less average.

5. "AlfaStrakhovanie"

It is included in the Alpha Group and is one of the system-forming Russian insurance companies. According to the company, a company is 1.4% of refusal. The average payment is 41,796 rubles, which is less than six thousand prices.

It is included in the Alpha Group and is one of the system-forming Russian insurance companies. According to the company, a company is 1.4% of refusal. The average payment is 41,796 rubles, which is less than six thousand prices.

4. "VSK"

The All-Russian Insurance Company is one of the largest in the country and even twice received gratitude from the President of Russia for the work done. In the Osago ranking, the insurance company ranks fourth (1.4% of failures). The average amount of insurance compensation is 42,180 rubles. Alas, the average price is more than 5.5 thousand.

The All-Russian Insurance Company is one of the largest in the country and even twice received gratitude from the President of Russia for the work done. In the Osago ranking, the insurance company ranks fourth (1.4% of failures). The average amount of insurance compensation is 42,180 rubles. Alas, the average price is more than 5.5 thousand.

3. "Max"

The Insurance Group "Max" was founded in the distant 1992. Then the working people of the Soviet peaceful atom of the Russian Federation needed health insurance services. Since 2007, "Max" insures employees of the Federal Customs Service, and in 2003 the company was provided with a master license. Although the level of failures at Max is one of the smallest - 0.8%, but the amount of average payout does not please - only 35,403 rubles, which is less than the average price for as many as 12 thousand rubles.

The Insurance Group "Max" was founded in the distant 1992. Then the working people of the Soviet peaceful atom of the Russian Federation needed health insurance services. Since 2007, "Max" insures employees of the Federal Customs Service, and in 2003 the company was provided with a master license. Although the level of failures at Max is one of the smallest - 0.8%, but the amount of average payout does not please - only 35,403 rubles, which is less than the average price for as many as 12 thousand rubles.

2. "Yugoria"

The shareholder of the Insurance Company "Yugoria" is the Government of the Khanty-Mansiysk JSC. However, "Yugoria" is not limited to the borders of the district: the company has a branched network of branches (about 60) and more than two hundred agencies presented in various regions of Russia. It has several subsidiaries specializing in different types of insurance activities, including life insurance and health insurance. According to the OSAGO, the "Yugoria" has only 0.7% of failures, so that it ranks second ranking. The average amount of payments - 44,051 rubles, which is three more than thousands less than the average market price.

The shareholder of the Insurance Company "Yugoria" is the Government of the Khanty-Mansiysk JSC. However, "Yugoria" is not limited to the borders of the district: the company has a branched network of branches (about 60) and more than two hundred agencies presented in various regions of Russia. It has several subsidiaries specializing in different types of insurance activities, including life insurance and health insurance. According to the OSAGO, the "Yugoria" has only 0.7% of failures, so that it ranks second ranking. The average amount of payments - 44,051 rubles, which is three more than thousands less than the average market price.

1. Jaso.

Heads the rating of insurance companies OSAGO in 2016 former "Railway Joint Stock Insurance Company". In 2015, it was evaluating the "exclusively high level of reliability" of the RAEX rating agency. And the truth is the percentage of reflaking OSAGO pays the smallest and is only 0.5%. The size of the average payment on the OSAGO is 44,992 rubles, which is less than the average price of three thousand rubles.

Heads the rating of insurance companies OSAGO in 2016 former "Railway Joint Stock Insurance Company". In 2015, it was evaluating the "exclusively high level of reliability" of the RAEX rating agency. And the truth is the percentage of reflaking OSAGO pays the smallest and is only 0.5%. The size of the average payment on the OSAGO is 44,992 rubles, which is less than the average price of three thousand rubles.

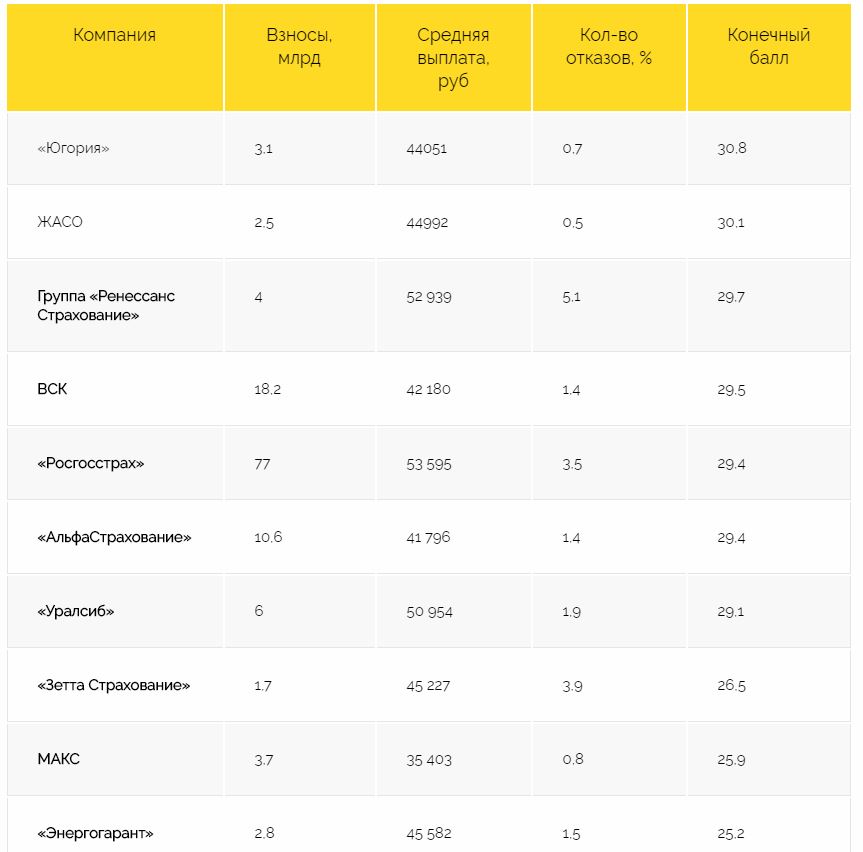

| Company | Contributions for OSAGO, billion rubles. | Middle payment on CTP, rub. | The number of failures in payments,% | Final score * |

|---|---|---|---|---|

| "Yugoria" | 3,1 | 44 051 | 0,7 | 30,8 |

| Jaso. | 2,5 | 44 992 | 0,5 | 30,1 |

| Renaissance Insurance Group | 4 | 52 939 | 5,1 | 29,7 |

| SPU | 18,2 | 42 180 | 1,4 | 29,5 |

| Rosgosstrakh | 77 | 53 595 | 3,5 | 29,4 |

| "AlfaStrakhovanie" | 10,6 | 41 796 | 1,4 | 29,4 |

| "URALSIB" | 6 | 50 954 | 1,9 | 29,1 |

| "Zetta Insurance" | 1,7 | 45 227 | 3,9 | 26,5 |

| MAX | 3,7 | 35 403 | 0,8 | 25,9 |

| Energogrand | 2,8 | 45 582 | 1,5 | 25,2 |

| SOGAZ | 7,8 | 42 872 | 6,9 | 23,8 |

| Ergo | 0,6 | 39 965 | 7,6 | 23,6 |

| "Reso-Warranty" | 27,6 | 43 796 | 4,8 | 23,5 |

| "Ingosstrakh" | 15,5 | 40 458 | 3,3 | 22,5 |

| "Consent" | 5,7 | 48 111 | 5,7 | 22,5 |

| "VTB Insurance" | 0,5 | 40 172 | 4,8 | 21,8 |

| "Alliance" | 0 | 65 766 | 9,1 | 21,4 |

| Insurance Group MSK | 0,3 | 43 868 | 6,1 | 19,6 |

| "Transneft" | 0,4 | 17 511 | 2,4 | 16,6 |

| "Capital Insurance" | 0,2 | 21 740 | 5 | 14,8 |

* - Given the CASCO data.

Leaders and outsiders

On the first line of the rating from 30.8 points was the company "Yugoria". It less often refuses to pay payments (in 2.6% of cases) and under the CTP (0.7%). At the same time, the average payout for CASCO from Yugoria is 68.7 thousand rubles, which is above the average value of 4.3 thousand rubles. But according to the Osago "Yugoria" pays, on the contrary, a little less than average - 44 thousand rubles. (The average value is 47.9 thousand rubles), but this did not prevent her heading the rating.

The CEO of Yugoria Alexei Okhlopkov said that this algorithm of assessment is quite objective and actually reflects the quality of execution by insurance companies assumed obligations. According to Okhlopkov, the main reason why "Yugoria" refuses to pay payments: "The event does not have signs of an insured event or the client is drawn without documents of the competent authorities during the second insurance case (in the first time it is permitted by the Company's rules)." The main reason for the refusal of the OSAGO - inactive the policy at the time of the accident.

Okhlopkov, however, considers a lack of methodology to use an average payout indicator - its low size can be associated with the features of the company's work with car services, if the client repairs the car at the expense of the company, and does not receive money in hand.

Of the 20 companies, eight pay better than the market average, and 12 worse. The worst result, according to RBC rating, has capital insurance. It was on the last line of the ranking with the final score of 14.8. A low assessment is related to the fact that the company very often refuses payments: 9.5% of the CASCO refusals and 5% - on the CCAMA. In addition, payments on the OSAO in "Capital Insurance" are twice as lower than the average and averaging and averaged 21.7 thousand rubles. However, the volume of fees on both types of insurance here does not exceed 1 billion rubles. The company does not respond to RBC request. Rosgosstrakh, which is in one group with "capital insurance", refused to comment.

The highest percentage of refusals in payments is "VTB insurance". The company does not pay 11.4% of those who applied for complaints on CASCO policies. The amount of payments in this type of insurance averages 88.4 thousand rubles. - More than the other 19 companies.

Deputy Director of the Company Evgeny Nisselson is surprised by the number of failures in the statistics of the Central Bank: "According to our internal data, the number of refusals to pay the CASCO polisses does not exceed 4%. The level of payments to customers - individuals is quite high. "

Error counties

Insurers criticize the calculation method. According to the head of the property insurance department and the auto insurance department of the Uralsib, Maria Barsoy, portfolios of insurance companies on CASCO and OSAGO can be very different from the company to the company, and this affects the amount of average payments on both types of insurance. "In one company, more expensive cars are insured, to the other - cheaper," she says. - Compare the amount of payments of these companies is not entirely correct. " According to her, the size of the average payments can affect the regional distribution of the contracts of contracts.

The head of the actuarial and methodological management of the "reso-guarantee" Maxim Shashlov says that insurers can take into account the costs of resolving insurance events in different ways (examination, evacuation, legal costs, etc.). "Some companies include them in the amount of payments, and some reflected separately in all reporting forms," \u200b\u200bsays Shashlov. Director of the Department of Analysis, Methodology and Control of the Insurance Company "Consent" Andrei Dyatlovsky notes that the calculations do not take into account all indicators of the quality of loss settlement: the share of payments for the court, the payload period, the number of complaints - that is, those who directly affect the complexity of obtaining compensation.

According to his colleague, Mikhail Petryaeva from the retail insurance management "ResH-Guarantees", evaluations do not take into account the growth of average payments due to court costs. Customers, if they are unhappy with the payment, appeal to the insurer, in this case, additional court costs fall. "Often, a higher average payment does not mean at all that customers received more money, as a significant part of the payment went on additional court costs," he believes.

The main criteria for estimating the ease of receipt of payments on CASCO should be the timing and quality of the car repair, says the representative of the retail insurance of the "reso-guarantee" of Ekaterina Zakharov. "Agreement with stations on the cost of repair, in particular spare parts, works and paints and varnishes, are influenced by the decline in payments, in particular parts, works. It is precisely the amount of average payments for the CASCO and the CTP, which at the "reso-guarantee" below the average market, did not give the company to get into the upper part of the rating.

"Insurers perceive absolutely any rating into the bayonets, because in muddy water it is easier to catch fish: now there are no guidelines on the market at all for the consumer, and companies do not need to make special efforts to fight for customers," explains the criticism of the Insurers Nikolai Nikaznikov from "Glavorschkontrol " He believes that the rating can be used as one of the criteria when making a decision on where to insure the car.

Almost every driver you want to buy mandatory insurance at a low price. There are many sentences here for 7,000 rubles, Tama 8000, and here at all for 1500. What is the reason for such a difference, and is it worth paying more? Which company is better to arrange the OSAGO?

Price ranger among insurance companies

The difference in the value of mandatory insurance among various insurers is approximately 20% and it is associated with the use of the price corridor. That is, it is allowed to calculate in the interval from the minimum base tariff to the maximum. On passenger cars - it is 3432 rubles. and 4118 rubles. respectively.

Also, the cost of the policy depends on the age of the driver, the experience, type TS and engine power, the region of residence, etc. For example, the young driver will cost more than experienced. And the resident of Moscow is cheaper than a citizen prescribed in St. Petersburg.

But if in the same settlement under the same conditions (age, experience, car, etc.) prices for insurers are distinguished, choose a cheaper option. The high cost is associated with the calculation at the maximum rate, rarely with the inclusion of additional services. From them you can refuse, it's a purely voluntary thing. Obligations In the other case, the insurer must fulfill in the desired volume.

Basic tariffs are installed at the state level, and insurance agents are not entitled to overestimate or underestimate them. Therefore, the price of 1500 rubles. On the motorway - a clear sign of the fake. Having bought it, the car owner risks himself to pay damage to the affected side, if an accident occurred by his fault. It is almost unrealistic to achieve insurance payments for such insurance.

So which company is better to make an OSAGO? In reliable, which will be able to fulfill its obligations in the required amount and within the prescribed period.

The most reliable insurers of Russia, or where better to buy OSAGO?

In our country there are many honest and decent insurers, but the top five includes:

Alfapture

Image 1: Alfactory logo.

Image 1: Alfactory logo.

One of the largest Russian insurers offering more than 100 insurance products for private and legal entities. There are over 270 regional offices. Located in the top ten insurers. Popted because of the favorable prices for CTP.

Reso-guarantee

Image 2: The logo of the reso-warranty.

Image 2: The logo of the reso-warranty. The company offers more than 100 types of insurance services. There are over 850 branches in the country. It is famous for a very rapid payment of payments.

Ingosstrakh.

Image 3: Ingosstraha logo.

Image 3: Ingosstraha logo. Based on the enterprise in the Soviet Union. It has more than 80 branches. It is possible to arrange a policy via a mobile application.

SPU

Image 4: VSK logo.

Image 4: VSK logo. There are more than 600 branches around the country. Reimburse losses within 5 days.

Rosgosstrakh

Image 5: Logo of Rosgosstrach.

Image 5: Logo of Rosgosstrach. Group customers are more than 26 million Russians. It has more than 3,000 branches.

Each company has bad and good reviews about each company. Someone complains about the imposition of additional services, others do not arrange the timing of damage compensation, etc. And to someone, on the contrary, liked the service speed, the cost of the policy, the possibility of making insurance in online mode, etc.

Decide where it is better to arrange the OSAGO, help. Use our service, compare the results and select the best option.

Brief comparison of insurers from the top five

Which company is better at the OSAGO? Ranking agencies are engaged in reliability. The most popular in Russia is "expert RT".

To assess the activities of the insurer, takes into account:

- Reliability.

- The size of the authorized capital.

From the first of July 1, 2003, a federal law entered into force, which ordered all car owners to arrange insurance on the OSAGO.

Dear readers! The article tells about the typical ways to solve legal issues, but each case is individual. If you want to know how solve your problem - Contact a consultant:

Applications and calls are accepted around the clock and seven days a week..

It's fast i. IS FREE!

Because the receipt of the OSAGA policy has become a prerequisite for all motorists, the question immediately arose, quite reasonable: "What kind of insurance company is best to conclude an agreement on the insurance of responsibility?".

The main factors when choosing an insurance company for which transport owners pay attention, are:

- efficiency and speed payment of compensation;

- high quality service;

- "Sarafan Radio" Reviews of friends, relatives, colleagues;

- the number of customers that are served in this company.

Not so long ago, the price of the policy was of great importance for motorists. But today's realities made their amendments, and this factor has ceased to be relevant.

What is Osago

OSAGO is, in fact, liability insurance. The main goal of the OSAGO-protection of the health and property of the motorist. In Osague, protection is focused on someone else's property and health, while the CASCO action extends to you and your car.

The purpose of the CTP is a mandatory compensation compensation for the affected side at an accident. The guarantor of payments is the state.

If the owner of the OSAGO policy became, then payments and compensation for insurance will receive the victim.

But the culprit of the accident repair his car or pay for his treatment will have to be "from its own pocket" with other types of insurance.

It is important to understand for yourself and remember that Osago covers costs only in the event of an accident. In other situations (hijacking, damage to the car in the parking lot, theft of things from the car) compensation of losses or damage to the CTP policy is not paid, since these events are not an insured event.

Damage is assessed by independent appraisers. This allows you to hope for a certain objectivity, but does not exclude complaints and issues on both sides of the accident.

The law prescribes to arrange the policy of the OSAGO for five days after the car in the property. Otherwise, the car is prohibited, and the traffic police will simply do not register it.

Policy Osague is competent in any region of Russia. At the request of the current legislation, the OSAGO policy must be issued for each car. In addition, it is impossible to arrange the policy at the same time.

Rating in Russia

Insurance services market is filled with many insurance companies. It is difficult for us to make a choice for yourself, with which one is most profitable to cooperate.

For insurance companies, the reputation in the services market is of great importance. If there is little about the company, only old customers will cooperate with it. It is in order to find out the real state of affairs in insurance companies and ratings are drawn up.

In order to decide which company to conclude an OSAGO Agreement to potential customers will have to explore the rating of insurance companies 2020 for the reliability of the CPP and only after that choose a reliable, comfortable and convenient insurance company.

In Russia, only a few agencies are evaluating the operation of the SC, they are ratings. Each of them has its own style and experience.

Therefore, the data of different RA may differ slightly from each other. For example, the national rating agency "NRA" is evaluated only to those SC, which voluntarily opened access to information about their activities.

- geography of the insurance company;

- the number of real customers;

- capital volume;

- interest ratio positive / negative solutions.

The data in the ratings is quite dynamic and constantly updated. This is due to the complex economic conditions of modernity. Companies facing financial difficulties, forced to revise the terms of contracts.

- financial stability;

- popularity among consumers;

- share of payments.

Price

The cost of CTP can be found directly in the insurance company, on the SK website or independently calculate it on the Calculator online.

| Insurance Company | Category, Type and Purpose of TC | Basic Insurance Tariff (rub.) |

| 867 | ||

| 3432 | ||

| 2573 | ||

| "C", "CE" less than 16 tons | 3509 | |

| "C", "CE" more than 16 tons | 5284 | |

| 2808 | ||

| 3509 | ||

| 867 | ||

| "B", "ve" for physical. Persons and IP | 4118 | |

| "B", "ve" for JUR. persons | 2573 | |

| "C", "CE" less than 16 tons | 3509 | |

| "C", "CE" is more than 16 tons | 5284 | |

| "D", "DE" up to 16 passengers | 2808 | |

| 3509 | ||

| "A", "M" Motorcycles, Mopeds, Light Quadrocycles | 867 | |

| "B", "ve" for physical. Persons and IP | 4118 | |

| "B", "ve" for legal entities | 2573 | |

| "C", "CE" less than 16 tons | 3509 | |

| "C", "CE" more than 16 tons | 5284 | |

| "D", "DE" up to 16 passengers inclusive | 2808 | |

| "D", "DE" more than 16 passengers | 3509 | |

| MSK | "A", "M" Motorcycles, Light Quadrocycles, Mopeds | 1579 |

| "B", "ve" for individuals and IP | 4118 | |

| "B", "ve" for JUR. persons | 3078 | |

| "C", "CE" less than 16 tons | 4211 | |

| "C", "CE" more than 16 tons | 6341 | |

| "D", "DE" up to 16 passengers | 3370 | |

| "D", "DE" more than 16 passengers inclusive | 4211 |

To independently calculate the cost of the CTP, you need to own the following information:

- know the type of vehicle (PTS,);

- know the power of the power plant in horsepower;

- know the place of official registration of the owner of the TC (civilian passport);

- specify the age of possible drivers (driver's license);

- know driver experience;

- know CBM (class) drivers.

Calculators for calculating the cost of CTP of some leading insurance companies:

- Rosgosstrakh;

- Ingosstrakh;

- Reso;

- Rosno.

Do not be afraid that the calculator "gives out" two numbers. This is the minimum and the maximum possible price of the Osago policy.

Such a price variation has become possible due to the fact that insurance companies have the right to independently establish the cost of the policy, within the limits of correction factors.

According to payments

When an insured event occurred, the company's customer is important to receive money on insurance. But all insurance firms carry out the allowed payments or do it inexpressive.

This table reflects the amounts that customers company have made as insurance for the year (fees); The amounts that were paid to people under insurance cases (payments) and the coefficient of devastability of the insurance event or the coefficient of cumulation (coefficient).

Similar words, this is the percentage of the number of affected customers of the company to the number of insurance events.

Table continuation:

By reliability

The level of reliability of insurance companies on expert estimates is measured in the following indicators:

- A ++ - an exceptionally high level;

- A + - very high level;

- A - high level.

National

- Can you recommend our friend service in this SC?

- Is the service of this insurance company convenient?

- Have you experienced difficulties in contacting this insurance company OSAGO?

| SC / Conditions | Payments (efficiency and amount) | Attitude to customers |

| Alpha - Insurance | 5 | 5 |

| VTB-protection | 5 | 5 |

| Ingosstrakh | 5 | 5 |

| Renaissance | 5 | 5 |

| SPU | 2 | 3 |

| Rosgosstrakh | 2 | 3 |

Table continuation:

| SC / Conditions | Evaluation of experts | Notes |

| Alpha - Insurance | 5 | The ability to issue a field on the road; Comfortable service |

| VTB-protection | 5 | Developed network of offices |

| Ingosstrakh | 5 | Transparent tariffs for OSAGO |

| Renaissance | 5 | Lack of additional "imposed" services |

| SPU | 5 | Rough attitude to customers; imposing additional services |

| Rosgosstrakh | 5 | Aggressive sales methods; overestimation of prices for services; Tightening payout |

The most popular SC in Moscow

| SK / Rating Level | Per (%) | Vs (%) | Official Rating |

| RESO WARRANTY | 78 | 22 | A ++. |

| Insurance house Voice | 60 | 40 | A ++. |

| Rosgosstrakh | 20 | 80 | A ++. |

| VTB Insurance | 0 | 100 | A ++. |

| PPF. | 50 | 50 | — |

| Alpha Insurance | 0 | 0 | A ++. |

| SOGAZ | — | 100 | A ++. |

But often the discontent of the clients is due not to the fact that the SK irresponsibly refers to his work, and by the fact that the customers themselves do not disturb themselves into the essence of the contract and carefully study it.

Choosing a company-insurer, anyone wants to be sure that upon the occurrence of the insured event, he will not be denied in due money. In order not to get into the unpleasant situation and save ourselves from the need to resolve disputes and settle the claims, it is worthwhile to learn the ratings of insurers before the conclusion of the Insurance Agreement.

To date, the most authoritative rating agencies specializing in the compilation of lists of insurance companies leading to the compliance of any criterion are the Expert RA and the National Rating Agency.

- the size produced by the company for a certain period of time;

- capital size of the insurer;

- evaluation of consumers, and both positive and negative feedback are taken into account.

Choosing an insurer, it is worth paying attention to the official ratings formed in the whole country. Repeat solely on public opinion about the company in a particular region or city is not worth it - it is often the result of a large-scale advertising campaign conducted by the insurer. At the same time, the quality of services provided, as a rule, does not comply with the stated promises.

- information is collected about the organization by conducting audits and personnel survey;

- the information obtained is analyzed, and an expert opinion is formed on their basis, on the basis of which the company ranks its place in the ranking.

If the insurer is satisfied with the assessment, he signs an agreement that allows you to publish the results of the inspection in open sources. Otherwise, he can appeal, the result of the satisfaction of which becomes the signing of an agreement on the non-disclosure of the information received. In the rating formed by the Agency, no information about this insurer will be made.

The gradation of the levels assigned by the results of the analysis is as follows:

- highest;

- very tall;

- tall;

- satisfactory;

- low;

- low;

- very low;

- unsatisfactory;

- failure to fulfill obligations;

- bankrupt company;

- liquidation of company.

Rating of the most reliable insurance companies as of 2020

Rosgosstrakh

The largest company on the scale of presence in the regions, the size of the assembled insurance premium, its own assets and reserves. In addition, this insurer produces the highest number of payments for various insurance cases. Included in the system-forming insurance companies in Russia.

SOGAZ

One of the largest Russian companies providing life insurance, health, autocarted responsibility, pension insurance, insurance against accidents, etc. Throughout the last five years, it is consistent in the first three of the most reliable companies.

Reso-guarantee

At the end of 2015, the company ranked third in terms of the assembled insurance premium, the size of which amounted to 77.875 billion rubles. At the same time, the total amount of insurance payments produced during the same period of time amounted to 40.168 billion rubles.

Ingosstrakh

The company is consistently among the top ten most reliable insurers providing insurance services in various spheres of human life. At the end of 2017, the size of the insurance premium collected by the company amounted to 71.1 billion rubles, which corresponds to the indicators of past years.

Alfapture

According to the results of 2017, the size of the assembled by the insurance premium amounted to 13.4 billion rubles; The amount of insurance payments for the same period amounted to 1.37 billion rubles. The company is widely represented in the regions of Russia: there are more than 270 representative offices in the country.

According to analysts, the troika of the reliability rating companies paid for about 35% of all insurance claims arising in the country in 2017. This means that the solvency of these insurers is at a high level and, upon the occurrence of an insured event, their customers can be confident that all payouts due to them will be fully implemented.

Choosing a company-insurer, it is worth paying attention to the rating assigned to it by authoritative rating agencies. Experts are advised to conclude agreements with companies with A ++ or A + ratings, which are currently the highest. The presence of such a rating in the insurer suggests that it has a sufficient number of assets and is solvent, which means that even if there are problems in the insurance market in the long run, they will be able to resist "afloat" and fulfill their obligations to customers. In total, as of 2020, these ratings have about two dozen insurers, including the companies listed above.