IN authorized capital firms can contribute not only money, but also any other property. The reflection of this operation in the accounting and tax accounting of the transferring and receiving parties has a number of peculiarities.

Lyubov DEMIDENKO

Auditor

The legislation of the Russian Federation provides for the possibility of making a contribution to the authorized capital of an economic company (joint-stock company or limited liability company) in the form of property that has a monetary value (Article 66 of the Civil Code of the Russian Federation, Articles 9, 34 Federal law dated 26.12.95 No. 208-FZ "On Joint Stock Companies", Art. 15 of the Federal Law of 08.02.98 No. 14-FZ "On Limited Liability Companies").

When making contributions to the authorized capital of property and non-property (non-monetary) contributions, the following is required:

• determination of the right to use property, securities, capital investments transferred as a contribution to the authorized capital of the company;

• determination of monetary compensation for property contributed to the account of a contribution to the authorized capital, for which the right to use has been terminated (for example, a lease agreement) and there is a need to return to the original owner;

documenting contributions of participants to the authorized capital of the company;

• expert assessment of objects contributed as payment for the participant's share (in some cases).

The monetary valuation of property contributed as payment for shares in the establishment of a joint-stock company or shares (contributions) in the authorized capital of an LLC is made by agreement between the founders. This decision must be taken by the founders unanimously. For example, such an assessment may be indicated in the memorandum of association between the participants of the LLC. When paying for additional shares of a JSC with non-monetary funds, the monetary value of the property contributed as payment for shares of the JSC is made by the board of directors (supervisory board) of the company.

Fixed assets, goods, materials, securities, etc. can be contributed to the authorized capital. In this case, the charter of a company may contain restrictions on the types of property that can be used to pay for shares of a JSC or a contribution to the authorized capital of an LLC.

To determine the market value of the property contributed as payment for shares, an independent appraiser must be involved. The value of the monetary valuation of the property made by the founders of the company and the board of directors (supervisory board) of the company cannot be higher than the value of the valuation made by an independent appraiser (clause 3 of article 34 of Law No. 208-FZ).

An independent appraiser is also involved in the appraisal of the property contributed to the authorized capital of the LLC. This happens if the nominal value of the share of a company participant in authorized capital LLC, paid with a non-monetary contribution, is more than 200 minimum wages (Article 15 of Law No. 14-FZ).

Accounting at the transmitting side

The contribution to the authorized (pooled) capital in the form of property is a financial investment of the organization (clause 3 of PBU 19/02 "Accounting for financial investments"; approved by order of the Ministry of Finance of Russia dated December 10, 2002 No. 126n). To reflect the contribution to the authorized capital, the Instruction on the Application of the Chart of Accounts for Accounting of Financial and Economic Activities of Organizations (approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n) provides account 58 "Financial investments", subaccount 1 "Shares and shares". The organization may reflect the accounting of preliminary costs for the acquisition of financial investments on a separate subaccount "Preliminary accounting of costs for the acquisition of financial investments", for example, 58-5.The disposal of assets as contributions to the authorized (pooled) capitals of other organizations is not recognized as its expenses (clause 3 of PBU 10/99 "Organization's expenses"; approved by order of the Ministry of Finance of Russia dated 06.05.99 No. 33n). Based on this, the payment of the contribution to the authorized capital in non-monetary funds in the investor's accounting is accompanied by the following entries:

Debit 58-5 Credit 01, 04, 08, 10, 41, 43, 58

- the book (residual) value of the property was written off;

Debit 91-2 Credit 76, 97, etc.

- the costs associated with the transfer of property are taken into account;

Debit 58-1 Credit 58-5

- reflected the contribution to the authorized capital.

Initial cost of the deposit

The initial value of financial investments contributed to the account of a contribution to the authorized (pooled) capital is their monetary value agreed upon by the founders (clause 12 of PBU 19/02). Note that the Regulation on accounting and accounting statements in Russian Federation(approved by order of the Ministry of Finance of Russia dated 07.29.98 No. 34n) prescribes to accept financial investments for accounting in the amount of actual costs for the investor (clause 44 of the regulation).The Ministry of Finance of Russia expressed its opinion on the collision arising in the regulatory documents on accounting in a letter dated 23.08.01 No. 16-00-12 / 15. In the opinion of the department, the accounting regulations and accounting regulations are normative legal acts of the same hierarchical level in the system of legal acts of the Russian Federation. Therefore, an act that came into force later takes precedence over a previously adopted document. Based on this, in our case, preference should be given to PBU 19/02.

It would be quite possible to agree with the above opinion of the Ministry of Finance of Russia, if not for paragraph 3 of the provisions on accounting. It establishes that the provisions on accounting are developed and approved by the department on the basis of the law on accounting and the Regulation on accounting and accounting in the Russian Federation. By this, the ministry, in our opinion, somewhat raised the level of the position on accounting in the hierarchy of normative acts in comparison with PBU. And it would still be more correct for the department to approve a new normative document, at the same time make the appropriate changes to the previously adopted ones.

Making a contribution to the authorized capital is not a gratuitous transfer of the contributed property. In return (in payment for this property), the contributing party receives a certain amount of property rights, consisting primarily of the right to receive a certain part of the profit earned by the company, and a certain part of its property in the event of the liquidation of the company. The conclusion about the non-gratuitous nature of the contribution to the authorized capital, which would seem obvious from the moment part of the first Civil Code of the Russian Federation came into force (January 1, 1995), was forced to be confirmed by the Presidium of the Supreme Arbitration Court of Russia (Resolution of 08.08.2000 No. 1248/00). Property rights (rights of claim against society), which the investor pays by making a contribution to the authorized capital, according to civil law, are a full-fledged type of property (Article 128 of the Civil Code of the Russian Federation). Thus, both parties - both the investor and the organization receiving the investment contribution - fulfill their obligations under this transaction in non monetary form... The procedure for assessing the income received from such transactions ("under contracts providing for the fulfillment of obligations (payment) with non-monetary funds"), including in connection with participation in the authorized capital of other organizations, is established by clause 6.3 of PBU 9/99. According to this clause, the amount of receipts and (or) accounts receivable under contracts providing for the fulfillment of obligations (payment) with non-monetary funds is accepted for accounting at the cost of goods (values) received or to be received by the organization. The cost of goods (values) received or to be received by an organization is established on the basis of the price at which, in comparable circumstances, the organization usually determines the cost of similar goods (values).

If we apply the procedure established by PBU 9/99 to the assessment of the value of property (shares) received as a result of payment for them with non-monetary funds, then the value of shares or the value of the corresponding receivables will be determined regular price acquisition of shares on the market at the time of foundation of the company. This price is equal to the price set by the company for the "placement" of shares, in general, identical to their par value. With regard to financial investments, the "amount of actual costs for the investor" will be equal in this case to the not traditionally understood cost of acquisition (residual value) of the property transferred as payment of a contribution to the authorized capital, but to the amount Money required to purchase this installment on the market. Consequently, the assessment of income in the form of the value of the property received does not in any way depend on the value of the property being retired.

Thus, a situation is possible when the property assessment agreed by the founders will not coincide with the book value of the transferred property according to the accounting data of the transferring party. In this regard, the question arises about the reflection of these estimates in accounting and, therefore, about the possibility of the appearance in it financial result from the operation of making (paying) a contribution to the authorized capital with non-monetary funds.

If the valuation of the property transferred to the authorized capital differs from its book (residual) value, then the transferor in accounting as a result of this business transaction forms a positive or negative balance. Economic essence of this financial result consists in obtaining a larger (smaller) volume of property rights in comparison with the value of the contributed property. For accounting purposes, the considered income (expense) the Ministry of Finance of Russia proposes to qualify as operational, associated with participation in the authorized contributions of organizations (letters of the Ministry of Finance of Russia dated 12.10.2000 No. 04-02-05 / 1, dated 23.03.2001 No. 04-02-05 / 1/61, etc.).

Example 1 According to the constituent documents, an object of fixed assets is transferred to the organization as a contribution to the authorized capital. Its book value is 350,000 rubles, the accrued depreciation amount at the time of transfer is 50,000 rubles. The cost of dismantling the facility amounted to 20,000 rubles.

Option 1. Debt on the organization's founding contribution - 200,000 rubles.

In accounting, the write-off of an object against the repayment of the debt on the constituent contribution is reflected as follows:

Debit 01 subaccount "Disposal of fixed assets" Credit 01

- 350,000 rubles. - the initial cost of the transferred object has been written off;

Debit 02 Credit 01 subaccount "Disposal of fixed assets"

- 50,000 rubles. - the amount of accrued depreciation has been written off;

- 200,000 rubles. - the cost of the object contributed to the authorized capital is reflected in the assessment in accordance with the constituent documents;

Debit 58-1 Credit 58-5

- 200,000 rubles. - reflected the contribution to the authorized capital.

Debit 91-2 Credit 01 subaccount "Disposal of fixed assets"

- 100,000 rubles. - reflected the operating expense for the object contributed to the authorized capital;

Debit 91-2 Credit 76

- 20,000 rubles. - reflects the costs of dismantling the object;

Loss on disposal of the object - 120,000 rubles. (100,000 + 20,000) will be taken into account when determining the balance of other income and expenses for the reporting month.

Option 2 З the organization's debts for the constituent fee - 500,000 rubles.

When the transaction is reflected in the accounting for the entry of the object into the account of repayment of the debt, the entries for writing off the initial cost of the object, the amount of depreciation and the costs of dismantling, given in option 1, remain (we do not repeat them). The rest of the entries will undergo changes:

Debit 58-5 Credit 01 subaccount "Disposal of fixed assets"

- 300,000 rubles. - the residual value of the object contributed to the authorized capital is reflected;

Debit 58-5 Credit 91-1

- 200,000 rubles. - reflected the operating income on the object contributed to the authorized capital;

Debit 58-1 Credit 58-5

- RUB 500,000 - reflected the contribution to the authorized capital.

Result from disposal of the object 180,000 rubles. (200,000 - 20,000) will be taken into account when determining the balance of other income and expenses for the reporting month.

________________________

End of Example 1

The moment of accounting for the deposit

The date and document on the basis of which the contribution to the authorized capital must be registered as a financial investment depends primarily on the type of business entity.When making a contribution to the authorized capital of an LLC, the date and document on the basis of which the financial investment is registered depends on the situation of making the contribution.

If a company is founded, then this moment will be the date of state registration in accordance with the procedure established by the federal law on state registration of legal entities (clause 3 of article 2 of law No. 14-FZ).

When increasing the authorized capital at the expense of additional contributions of its participants and contributions of third parties accepted into the company, it is the day of state registration of the corresponding changes in the constituent documents of the company by the body carrying out state registration legal entities (clauses 1, 2, article 19 of Law No. 14-FZ).

If a share is acquired from a participant in an LLC, then the financial investment is reflected in the accounting at the time of the written notification of the company about the assignment of the share (part of the share) in the authorized capital of the company with the presentation of evidence of such an assignment (clause 6 of article 21 of Law No. 14-FZ) ...

The date and document on the basis of which a financial investment is registered when paying with property for the company's shares depends on the form in which they are issued: documentary or uncertified.

In the case of a documentary form of shares, such a moment is the date of transfer to the owner of the shares of their certificate (which will be the necessary primary document) after the entry is made on the personal account of the acquirer in the register of shareholders.

If the shares are issued in non-documentary form, then financial investments are accepted at the time of making a credit entry or according to the acquirer's depo account (in the case of accounting for rights to securities from a person carrying out depository activities) or on the personal account of the acquirer in the case of accounting for rights to securities in the register keeping system on the basis of an extract on the corresponding account (Articles 28, 29 of the Federal Law of 22.04.96 No. 39-FZ "On the Securities Market ").

VAT

When transferring property in the form of a contribution to the authorized capital, the procedure for calculating with the budget for VAT depends on the purpose for which this property was previously acquired: for investment purposes (i.e. directly for transferring it as a contribution to the authorized capital or to pay for shares) or for other transactions recognized as objects of VAT taxation.As you know, transactions on the transfer of property to the authorized capital of business entities and partnerships are not recognized as the sale of goods (works, services) (subparagraph 4 of paragraph 3 of article 39 of the Tax Code of the Russian Federation). Proceeding from this, this operation is not recognized as an object of VAT taxation (subparagraph 1 of paragraph 2 of article 146 of the Tax Code of the Russian Federation). The amounts of VAT presented to the buyer when purchasing goods (works, services), including fixed assets and intangible assets, are taken into account in their cost in the event of their acquisition for the production and (or) sale of goods (works, services), sales operations ( transfer) which are not recognized as the sale of goods (works, services) in accordance with paragraph 2 of Article 146 of the Tax Code of the Russian Federation (subparagraph 4 of paragraph 2 of Article 170 of the Tax Code of the Russian Federation). Thus, when purchasing property for investment purposes, the amount of VAT paid to the seller is included in its initial value.

When acquiring property for transactions subject to VAT, the amount of tax paid to the buyer at the time of its acquisition is deducted if the relevant conditions determined by Articles 171 and 172 of the Tax Code of the Russian Federation are met, namely: the presence of an invoice, documents confirming the payment of tax amounts, and property registration. Deductions of tax amounts presented by sellers to the taxpayer when purchasing fixed assets and intangible assets are made in full after they are registered.

If the taxpayer has accepted for deduction the VAT paid to the supplier on goods (works, services) used for operations for the production and sale of goods (works, services) that are not subject to VAT, the corresponding tax amounts are subject to recovery and payment to the budget (p. 3 article 170 of the Tax Code of the Russian Federation).

Previously, the tax authorities, based on this norm, obliged taxpayers to recover VAT on property transferred to the authorized capital in the tax period in which the transfer was made, in terms of its value, which is not included through depreciation deductions in the costs of production and (or) sale of goods (works). , services) or non-operating expenses taken into account when determining income tax (clause 3.3.3 of the Methodological Recommendations for the Application of Chapter 21 "Value Added Tax" of the Tax Code of the Russian Federation; approved by order of the Ministry of Taxes and Levies of Russia dated 20.12.2000 No. BG-3-03 / 447). However, by order of the Ministry of Taxes and Tax Collection of Russia dated 11.03.04 No. BG-3-03 / 190, this “wish” was excluded.

It is possible that the change in their position was also influenced by the resolution of the Presidium of the Supreme Arbitration Court of Russia dated 11.11.03 No. 7473/03. The tax authorities' demands for additional VAT charges in a similar situation were recognized as unlawful, since tax legislation does not contain a requirement for subsequent reimbursement to the budget of the tax amount accepted for deduction when registering fixed assets after transferring them to the authorized capital of another business company.

Based on the foregoing, the organization must independently decide on the restoration of the amount of previously credited VAT. If the organization nevertheless decides to restore VAT, then this is reflected in the accounting records by the following entries:

Debit 19 Credit 68 subaccount "Calculations for VAT"

- VAT on the transferred property has been restored.

The amount of VAT recovered from the budget, according to the author, should increase the cost of the actual costs of acquiring a share in the authorized capital:

Debit 91-2 Credit 19

- the amount of the restored VAT is reflected.

income tax

The expenses of the investing organization in the form of contributions to the authorized capital of another organization are not taken into account when calculating profit tax (clause 3 of article 270 of the Tax Code of the Russian Federation).Not recognized as profit (loss) of a taxpayer-shareholder (participant, shareholder) is the difference between the value of property contributed as payment, property rights and the par value of the acquired shares (stakes, shares) subparagraph 1, clause 1 of Art. 277 of the Tax Code of the Russian Federation). Consequently, the profit (loss) reflected in the accounting, which was formed when contributed to the authorized capital, is not taken into account when calculating income tax.

The cost of acquired shares (stakes, units) for tax purposes is recognized as equal to the value (residual value) of the contributed property (property rights), determined according to tax accounting data as of the date of transfer of ownership of the specified property (property rights), taking into account additional costs that for the purposes of taxation are recognized by the transferring party upon such introduction (clause 1 of article 277 of the Tax Code of the Russian Federation). Additional costs can be the costs of dismantling, transportation of property, etc., as well as the recovered amount of VAT (if any).

Thus, the value of shares (stakes, units), reflected in the accounting records according to the valuation agreed by the founders, may not coincide with the value of the same shares (stakes, shares) recorded in tax accounting at the residual value of the property contributed to the authorized capital, taking into account additional costs incurred by the transferring party when the property is contributed to the authorized capital.

In the event of further sale of these shares (stakes, units) for the purpose of calculating income tax, an expense in the amount of the residual value of the property transferred as payment for the contribution (shares) will be accepted as a decrease in income.

Example 2 Consider tax implications transfer of an item of fixed assets, using the data of example 1, assuming that the value of the transferred item for accounting coincides with its residual value in tax accounting.

Option 1... In the tax accounting register, in which the investor organization keeps records of the acquired shares (stakes, units), the value of the share in the authorized capital is reflected in the amount of 320,000 rubles. (300,000 + 20,000).

The difference between the par value of the acquired share in the authorized capital of the company and the value of the object contributed as payment is a loss of 120,000 rubles. (200,000 - 320,000) is not included in expenses when calculating income tax in the current reporting (tax) period.

If in the future this share is sold at the cost of 200,000 rubles established by the founders, then the above-mentioned loss of 120,000 rubles is taken into account when calculating income tax.

Option 2... The cost of the share in the authorized capital does not change in comparison with option 1 - 320,000 rubles.

The difference between the nominal value of the acquired share in the authorized capital of the company and the value of the object contributed as payment is a profit of 180,000 rubles. (500,000 - 320,000). It is not taken into account as part of income when calculating income tax in the current reporting (tax) period.

With further implementation of this share at the cost established by the founders of 500,000 rubles. when calculating income tax, the aforementioned profit of 180,000 rubles is taken into account.

Assuming that the value of the property in tax accounting is zero, then the values accepted in tax accounting when calculating income tax will change.

Option 1... The value of the share in the authorized capital is entered in the tax register - 20,000 rubles. (0 + 20,000).

The difference between the par value of the acquired share in the authorized capital of the company and the value of the object contributed as payment is profit in the amount of 180,000 rubles. (200,000 - 20,000) is not included in income when calculating income tax in the current reporting (tax) period.

With further implementation of this share at the cost established by the founders of 200,000 rubles. when calculating tax in income, the amount received above is taken into account 180,000 rubles. (profit).

Option 2... The cost of the share in the authorized capital is the same - 20,000 rubles.

The difference between the nominal value of the acquired share in the authorized capital of the company and the value of the object contributed as payment is profit in the amount of 480,000 rubles. (500,000 - 20,000) is not included in income when calculating income tax in the current reporting (tax) period.

With the further sale of this share at a cost of 500,000 rubles. when calculating income tax, the above profit of 480,000 rubles will be taken into account in income.

____________________________

End of Example 2

When transferring securities to the authorized (pooled) capital, the tax base of a shareholder is established in accordance with the specifics of determining the tax base for income received from the transfer of property to the authorized (pooled) capital (fund) of an organization, which are defined by Article 277 of the Tax Code of the Russian Federation. This article establishes that the difference between the value of the property, property rights contributed as payment and the par value of the acquired shares (stakes, shares) is not recognized as profit (loss) of the taxpayer - shareholder (participant, shareholder) during the placement of issued shares (stakes, shares).

When transferring property to the authorized capital, the transferring party's contribution is assessed at the property's value accounted for in the transferring party's tax accounting records. If securities are transferred, then their value is determined as the purchase price, increased by the costs associated with the purchase of securities, that is, without taking into account the value of the securities contributed to the authorized capital, carried out by an independent appraiser and agreed with other members of the established organization. Note that the provisions of Article 280 of the Tax Code of the Russian Federation do not apply to the transfer of securities to the authorized capital.

Differences in the reflection of the transaction for making a contribution to the authorized capital in the form of property in accounting and tax records oblige organizations to refer to the norms of PBU 18/02 "Accounting for calculations of income tax" (approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n).

Failure to recognize for tax purposes the profit (loss) associated with the appearance of a difference between the assessed value of the property when it is entered into the authorized (pooled) capital of another organization and the value at which this property is reflected in the balance sheet of the transferor, leads to permanent differences if in the future, the sale of shares (shares, units) is not provided. In this case, it is necessary to calculate a permanent tax liability in accounting (clauses 4 and 7 of PBU 18/02). Since the magnitude of the constant differences can take both positive and negative values, the "derivative" of them will also have the same sign.

Of course, it would be more logical to use the term “permanent tax asset” if the constant tax liability is negative. But, unfortunately, the developers of PBU 18/02 did without it, although this term is used in the recommended form No. 2 "Profit and Loss Statement" (Order of the Ministry of Finance of Russia dated July 22, 2002 No. 67n).

The accrual of a positive amount of a permanent tax liability is accompanied by the entry:

Debit 99 subaccount "Permanent tax liability" Credit 68 subaccount "Calculations of income tax"

- a permanent tax liability has been accrued.

With a negative value of the permanent tax liability (permanent tax asset), a reverse posting is made:

Debit 68 subaccount "Calculations of income tax" Credit 99 subaccount "Permanent tax liability"

- a negative permanent tax liability (permanent tax asset) has been accrued.

If the organization contributes property to the authorized capital with the aim of further implementing the shares (shares, shares), then the above differences in accounting and tax accounting form temporary differences. The profit (loss) associated with the appearance of a difference between the assessed value of the property when it is entered into the authorized (pooled) capital of another organization and the value at which this property is reflected in the balance sheet of the transferring party is not included in tax accounting in the current reporting (tax) period. accounted for, but accounted for in the future in the reporting (tax) period, when the sale of a share (shares, shares) takes place. At the same time, depending on the ratio between the assessed value of the property and the value at which this property is reflected in the balance sheet, both deductible temporary differences and taxable ones may arise. Each of them obliges the organization to charge:

• deferred tax asset - for a deductible temporary difference;

• deferred tax liability - for taxable temporary differences.

Their accrual is accompanied by records:

Debit 09 Credit 68 subaccount "Calculations of income tax"

- a deferred tax asset has been accrued;

Debit 68 subaccount "Calculations of income tax" Credit 77

- a deferred tax liability has been accrued.

When selling shares (shares, shares), reverse entries are made:

Debit 68 subaccount "Calculations of income tax" Credit 09

- the deferred tax asset has been written off;

Debit 77 Credit 68 subaccount "Calculations of income tax"

- the deferred tax liability has been written off.

Receiving party accounting

According to the Chart of Accounts of accounting, the receipt of deposits in the form of fixed assets, intangible assets, tangible assets, securities is reflected in the records:Debit 08, 10, 58 Credit 75 "Settlements with founders".

- reflects the contributions made by the founders in non-monetary form.

The objects of assets contributed to the account of contributions to the authorized capital of the organization are assessed at the cost agreed by its founders (participants), taking into account the actual costs of the organization for their delivery and bringing them into a condition suitable for use (clauses 8, 11 PBU 5/01, p. 9, 12 PBU 6/01, p. 9 PBU 14/2000, p. 12 PBU 19/02).

Depreciation on the fixed assets contributed to the deposit account is charged in accordance with the generally established procedure, starting from the 1st day of the month following the month of accepting this object for accounting, during the period useful use an object determined when the object is accepted for accounting (17, 20, 21 PBU 6/01) with its attribution to expenses for ordinary activities or others.

The value of the property received may not be equal to the value of the shares (stakes, shares) of the company. The obligation to calculate tax does not arise both in relation to the value of the property received, which is equal to the contribution, and in the amount of the excess of the value of the property over the contribution (share premium). Since when calculating the tax base for income tax, income in the form of property, property or non-property rights that have a monetary value, which are received in the form of contributions (contributions) to the authorized (pooled) capital (fund) of the organization (including income in the form of excess of the placement price shares (stakes) over their par value (original size)) are not taken into account (subparagraph 3 of paragraph 1 of article 251 of the Tax Code of the Russian Federation). The taxpayer-issuer does not recognize as profit (loss) the difference between the par value of the placed shares (stakes, shares) and the value of the property received (including cash), property rights, when the taxpayer places the shares (stakes, shares) issued by the taxpayer (subparagraph 1, p. . 1 article 277 of the Tax Code of the Russian Federation).

Thus, the question of taxation at the time of receipt of property as a contribution to the authorized capital does not arise. At the same time, there remains the question of determining for tax purposes the value of the property received as a contribution to the authorized capital.

The Tax Code of the Russian Federation does not contain a rule determining at what value a given property should be accounted for in tax accounting with the receiving party. The tax authorities set out their vision on this issue in Methodical recommendations on the application of Chapter 25 "Corporate Profit Tax" of the Tax Code of the Russian Federation (approved by order of the Ministry of Taxes and Duties of Russia dated 20.12.02 No. BG-3-02 / 729). So, in section 5.3 it is said that fixed assets received in the form of a contribution (contribution) to the authorized capital of an organization for tax purposes are accepted at the residual value of fixed assets received as a contribution to the authorized capital of the object of fixed assets, which is determined according to tax accounting data from the transferring party. ... In section 7.2.7 of the recommendations, it is indicated that when transferring property to the authorized capital, the contribution of the transferring party is assessed at the value of the property recorded in the tax accounting of the transferring party. In the same assessment, the property is taken into account in the tax accounting of the receiving party, the value of which must be documented. Before the publication of the methodological explanations, the opinion of the tax authorities was somewhat different. The initial value of the fixed assets contributed to the account of the contribution to the authorized capital of the organization was recognized as their monetary value, agreed upon by the founders (participants).

According to the author, the tax value of the property received as a contribution to the authorized capital should be equal to the tax value of this property from the transferring party. The following can be suggested to substantiate this conclusion. Subparagraph 2 of paragraph 1 of Article 277 of the Tax Code of the Russian Federation states that the value of acquired shares (stakes, shares) for tax purposes is recognized as equal to the value (residual value) of the contributed property (property rights), determined according to tax accounting data on the date of transfer of ownership of the specified property (property rights). However, this rule directly concerns the transmitting side. But if the tax value of the shares is estimated based on the tax value of the transferred property from the transferring party, then it can be assumed that the tax value of the same property from the receiving party should be the same. Therefore, it is advisable for the organization receiving the property as a contribution to request from the transferring party a certificate of its tax value.

Nevertheless, given that all irreparable doubts, contradictions and ambiguities in the acts of legislation on taxes and fees are interpreted in favor of the taxpayer (clause 7 of article 3 of the Tax Code of the Russian Federation), the organization has the right to independently make a decision on the assessment of the property received in tax accounting: according to the agreed by the founders or at the tax residual value of the property, determined at the time of its transfer to the authorized capital from the transferring party.

If the organization's value of the property received in payment for the contribution in tax accounting does not coincide with its value in accounting, then when making a contribution of depreciable property - monthly, for other property - at the same time at the time of its write-off there will be permanent differences. And they, as mentioned above, will oblige the organization to charge a permanent tax liability. And this, in turn, will entail the use of the above postings:

Electricity consumption without a contract: how to avoid negative legal consequences. Organizer: Higher School of State Audit of Moscow State University

Property, along with cash, can be transferred for the purpose of depositing into. The main point is that the property must be for equivalence to cash, that is, the specialist makes an expert decision on the market value of the transferred property.

Is it possible to contribute to the Criminal Code with non-monetary funds

According to the Civil Code of the Russian Federation, the authorized capital of economic entities can be formed either at the expense of any property. However, significant changes introduced in 2014 determined new rules for the formation of the authorized capital. According to them, enshrined in legislation for various legal entities should be formed only at the expense of funds. Capital that is deposited in excess of the established limit can be presented in the form of non-monetary property, which is valued in monetary terms.

The property transferred as a contribution can have a wide variety of uses. For example, it can be inventory items, which are subsequently used in the implementation of production process... Also, securities can be accepted as a contribution, which, with proper investment portfolio management, can bring tangible income.

The procedure for contributing to the authorized capital of property

If the investor has decided to contribute his property as a contribution to the authorized capital, he must go through the procedure established by law. It lies in the implementation following operations as from the side natural person, and on the part of an economic entity:

- must determine what part of the authorized capital will be formed at the expense of the contributed property, and which - at the expense of monetary funds. Do not forget that the monetary part must be at least the minimum amount established by law. The rules for the formation of capital, including at the expense of property, should be reflected in the constituent documentation - and the memorandum of association;

- an individual - a participant wishing to transfer property to contribute to the authorized capital, must organize an independent assessment of the transferred property. This is necessary in order to determine how much monetary units the transferred contribution corresponds.

Monetary valuation should be carried out by an independent appraiser, who forms his opinion in the form of a valuation report. The assessment by an independent expert is a mandatory point, since he will not have any bias in his work, and, therefore, will guarantee the reliability of the information provided.

The choice of an independent appraiser should be carried out carefully, and at the same time, check the availability of appropriate documents for the possibility of carrying out this activity, otherwise the results of this assessment will be invalid. The documents confirming the right to operate include documents on special education, a certificate of admission to an SRO, a liability insurance policy and an agreement for an independent assessment.

The appraisal report must be submitted to the registration authorities, both at the initial registration of the authorized capital, and when registering its changes in the direction of increase. It is not required to submit an appraisal report to the tax authorities;

- the property that is transferred by the owner in the form of a contribution to the authorized capital must have appropriate ownership documents. An individual is obliged to transfer documents to the property as proof of ownership, and entity must check them for authenticity;

- property transferred as a contribution is drawn up by the appropriate act of acceptance and transfer, which reflects all the necessary information. It includes the full name of an individual and, a description of the transferred property, its characteristics and quantity, as well as, most importantly, the cost according to an independent assessment;

- after the act of acceptance and transfer of property is signed by both parties, the property is put on the balance sheet of the organization on the appropriate accounts, for example, for accounting for fixed assets or, inventory, finished products or financial investments.

How to divide the property contributed to the authorized capital? Watch in the video below:

Free transfer

If the owner transfers his property in order to contribute to the authorized capital, this does not mean at all that it is handed over free of charge, that is, it is completely alienated. When the investor gives up the property, in return he acquires property rights, according to which he has the right to a certain part received profit.

If the depositor expresses a desire to withdraw from the founders, the property transferred earlier is returned to him. In a situation where such property cannot be reimbursed, it is also possible. Here, the previously conducted independent property assessment, which expresses the monetary equivalent, may come in handy - it will need to be transferred to the participant upon leaving the composition.

According to the law, each of the founders is obliged to contribute to the capital (authorized) a monetary amount equal to his share. The amount can be expressed not only in monetary form, but also in material values. This norm is regulated by law number 14-FZ article 15 paragraph 1.

Features of making in-kind contributions to the Criminal Code

Advantages

There are several advantages of replenishing a company with a non-cash asset:

- Items or equipment that is necessary for conducting business transactions, including entrepreneurial activity(such as a computer or printer).

- Items can enter the company's balance sheet from the founder if he has a certain stock (including illiquid stock), in which case the appraiser also evaluates it at market value.

- To conduct commercial transactions with this product or property (including real estate). For example, a company can sell the received product, leaving the realized funds for itself.

Requirements

The minimum amount of the contribution made for the forms of ownership of the LLC is 10,000 rubles, which must be paid exclusively in cash. Everything else can rightfully be covered by objects, real estate, movable property (), jewelry, equipment, goods, raw materials. The company prescribes those categories of property that can be accepted as a constituent contribution.

There are general legal restrictions that do not allow the following elements to be transferred to capital:

- Right to use land plot;

- The right to lease land plots located in the forest zone;

- The right to operate a land plot that was transferred by the state to a resident of the EIA (special economic zone);

When transferring non-monetary funds to a company with limited liability, the founder is obliged to grant ownership.

In some cases, a temporary transfer for a specified period is possible. This is separately described in the asset transfer and acceptance certificate. The normative score is also indicated.

We will talk about how you can assess the property-contribution to the authorized capital below.

Assessment of property contributed to the authorized capital

For assets that are provided to a limited liability company with a total nominal value of less than 20,000 rubles, an opinion of an independent expert appraiser is required. Until 2014, items with a specified value or less were evaluated by a general meeting of all members of the society. A unanimous vote was required to make a decision. Today, when transferring any asset, it is necessary to carry out a legally confirmed valuation from an independent appraiser.

- The final conclusion is influenced by market factors that developed at the time of the examination. The basis is the conditions under which this property can be sold at the time of the appraisal in free conditions. The final result is documented.

- Some appraisers do not conduct a physical examination of items, but make an expert opinion based on the photos sent, technical parameters and other documents that could confirm the final result.

About who evaluates the value of the contribution to the authorized capital of the property, read below.

Appraiser selection

An organization that can conduct an expert assessment must be registered with an SRO. The list of companies officially entitled to carry out activities on the expert setting of the market value of property is presented in the Russian state register.

The cost of services from companies depends on the item itself and its volume. For a laptop, the amount can reach a thousand rubles, and for a land plot or a package of securities - up to 50 thousand rubles. The examination time takes about one week or several days for oversized types of computer equipment.

According to Article 16 of the Federal Law No. 135, an appraiser has no right to be related to one of the founders or not to be a creditor (debtor) of the aforementioned persons.

We will describe below how the monetary valuation of the property contributed to the authorized capital proceeds.

Procedure

The evaluator uses information from the public domain to draw parallels with similar offers on the market. All are counted specifications and operating conditions. The process of drawing up an act for securities and other elements that have an actual established value has been simplified as much as possible.

Additional conditions for making a contribution to the authorized capital are determined by the Articles of Association of the company. The process of this procedure may be prescribed there. If the details are not set in the main document of the LLC, then you should adhere to legislation, according to which the maximum term for making a contribution after its assessment is four calendar months.

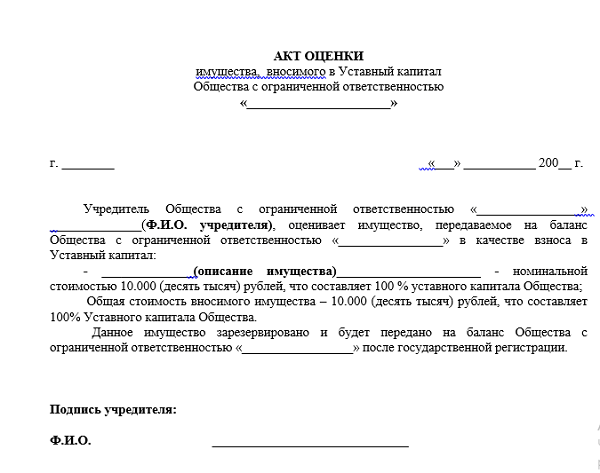

An appraisal report (sample) of the property contributed to the authorized capital is possible.

The act of appraisal of the property contributed to the authorized capital

The procedure for adding property to the authorized capital after the assessment is discussed below.

The procedure for making such a contribution

- After choosing an expert or a company, an appropriate contract for the provision of services is concluded. Such a sample does not have a strict established form. The SRO, where it is located, is considered to be mandatory.

- There is a process of transferring information about an object or object.

- The appraiser issues an act containing information about the potential value. The board of founders must approve it within six months from the date of its drawing up by the appraiser (the boundary period of the act).

- The charter prescribes the amount specified in the act.

- An act of acceptance and transfer is drawn up and the property becomes the property of a limited liability company.

The last action that must be taken is to submit the appropriate act to the state fiscal service. If desired, later, it is possible to increase the authorized capital by property (with its preliminary assessment).

The video below will tell you about the assessment of the contribution to the authorized capital of the property:

When an enterprise is created, its founders contribute a certain amount, which forms the authorized capital of the organization. This contribution of finance or property to the authorized capital is necessary in order for the organization to be able to operate on legal grounds... The amount to be paid is determined at the state level. In the event that one of the co-founders of the firm wishes to leave the ranks of its co-founders, then he has the right to demand the return of the amount he contributed to the general treasury.

When an organization is already functioning, changes in the amount of its authorized capital can occur both upward and vice versa. But any manipulations must be officially reflected on paper.

In this article

Property contribution to the company's fund

When establishing a company, there can be several or only one participants. In the event that several people have decided to become co-founders of the organization, they contribute their shares to the authorized capital, which is noted in the Minutes of the general meeting of founders. When a company is created by a citizen alone, then a note on the introduction of property is made in the Decision on the creation of an enterprise.

According to the current legislation (), a contribution to the authorized capital of an enterprise can be in the form of movable and immovable and property. Moreover, all real estate is subject to mandatory state registration.

In any situation, when determining property in the authorized capital, it must have a monetary value. This assessment approved by all founders and displayed in the minutes. If the amount exceeds 20 thousand rubles, the involvement of independent appraisers is required.

It should be understood that the property that was included in organization fund, after passing the registration procedure, will be recognized as the property of the company. The contributed property must be transferred to the company no later than 4 months from the moment the enterprise was established. When the founder does not pay his share within the specified period, it becomes the property of the organization.

It should be understood that the property that was included in organization fund, after passing the registration procedure, will be recognized as the property of the company. The contributed property must be transferred to the company no later than 4 months from the moment the enterprise was established. When the founder does not pay his share within the specified period, it becomes the property of the organization.

Procedure for depositing property

In addition to crediting financial resources to the fund of the company, you can also make a share in the authorized capital with property. To implement this opportunity, you will need to collect certain documents:

When it comes on the creation of a limited company, then the contribution of the minimum property to the authorized capital of an LLC during creation cannot be less than 10 thousand rubles. Moreover, only half of the amount can be deposited at a time, and the remaining part can be paid during the first year of the enterprise's operation.

When one person acts as the founder, then the decision on the value of the property is made by him alone. All standard documents that are used at the enterprise for these purposes can be adjusted specifically for a specific institution. But for this, you should first consult with lawyers.

When one person acts as the founder, then the decision on the value of the property is made by him alone. All standard documents that are used at the enterprise for these purposes can be adjusted specifically for a specific institution. But for this, you should first consult with lawyers.

In order to transfer property from the founder to the balance of the institution, it is necessary to draw up an act of transfer. It must be signed by each of the co-founders.

It should be understood that when drawing up the constituent document, it is very important to note in it the possibility of depositing property as authorized capital. In addition, restrictions on specific types of objects are also noted.

The property contribution to the authorized capital is not a gratuitous transfer. This means that the founder has the opportunity in the future to receive a share of the profit proportional to the contributed part of the property, which will be earned by the organization.

How property is displayed on the balance sheet

The current regulatory enactments determine that there will be no difference between the form in which assets were received on the balance sheet of the organization. In order for values to be displayed on the balance sheet as fixed assets, certain requirements must be met:

- the asset is used for a period of more than one year;

- the subsequent resale of such an asset is not provided;

- using the received asset, the company will be able to make a profit in the future;

- the contributed property object during the direct activity of the enterprise can be used both for performing targeted works and for management activities.

Subject to the correspondence of the contributed values to all specified requirements they can be attributed to the fixed assets of the enterprise. The property can be accounted for as low-value investments, as well as profitable investments. All these nuances should be reflected in the enterprise policy.

Subject to the correspondence of the contributed values to all specified requirements they can be attributed to the fixed assets of the enterprise. The property can be accounted for as low-value investments, as well as profitable investments. All these nuances should be reflected in the enterprise policy.

If we talk about the taxation of that property, which is contributed to the authorized capital of the company, then in 2017, for enterprises operating on a simplified system, the following standards will apply:

- the taxable amount of the company's income will not be increased;

- will not apply to expenses, according to article 346 of the Tax Code of the Russian Federation, since for organizations on a simplified system, paid expenses are not considered expenses.

If fixed assets are to be written off, then the situation is somewhat different:

- property that entered the company's balance sheet for the first time will not be attributed to its income part, in accordance with Article 251 of the Tax Code of the Russian Federation;

- for the procedure for writing off values, it will be required from the founder of the company to obtain a material valuation of the asset. In addition, an independent appraiser is also involved, who makes his own verdict.

In a situation where the value of assets is less than 100 thousand rubles, the organization has the opportunity to write them off at the same time when commissioning takes place, or in stages - within one reporting period. According to article 254 of the Tax Code of the Russian Federation, this can be done in the accounting of mat expenditures. Here the choice will be directly for the taxpayer. When their value does not exceed 40 thousand rubles, it is written off immediately, upon commissioning, when it comes to writing off assets for income tax.

The same assets, the value of which will be more than one hundred thousand rubles, will necessarily be attributed to property subject to depreciation.

It should be understood that any manipulations must be reflected in the relevant accounting documentation of the enterprise.

The authorized capital is a certain amount of money invested by the founders of the enterprise at the time of its creation. This is the minimum amount of property for conducting statutory activities. Minimum size capital is established by law. The authorized capital, among other things, characterizes the property of all founders, who, in the event of withdrawal from the owners, may demand the return of the contributed share in cash.

In the process economic activity the size of the authorized capital may well change - increase or decrease. All changes that occur are registered in the constituent documents without fail.

About shares of the authorized capital

If the number of founders of the organization is more than one, then the entire authorized capital is divided into shares, determined as percentages or fractions. The actual value of the participants' shares is proportional to the shares of the net asset value. So, for example, if the participant's share is 20%, and the amount of assets is 100 thousand rubles, then the value of the participant's share is 20 thousand rubles.

The decision to increase the authorized capital may be made due to the insufficient number of working capital, licensing requirements or the entry of new members who also contribute. But such an increase in the authorized capital is not allowed in all cases.

The increase is made at the expense of the following funds:

- property of the organization,

- by contributing additional funds by the "old" participants,

- by depositing funds by new members.

In the event of an increase in capital at the expense of contributions from all members of the organization, a decision on this is made at the general meeting. The protocol contains the total amount of the deposit, as well as the ratio of the amounts due to the increase in the share of participants.

If a contribution is accepted from a third party wishing to become a member of the company, then an application for joining the company is considered first, as well as for making a contribution with all the detailed accompanying information. Then a positive decision is made in the same way at the general meeting.

The fact of an increase in the authorized capital of the organization is registered by the appropriate government agency as a change in the constituent documents. Joint-stock companies are also obliged in this case to issue an additional block of shares.

About depositing property

As a rule, the authorized capital of the company being founded is supported by means of a savings bank account. But, as can be seen above, it can be brought in with any other property, which can be fixed assets, any securities, materials, goods, etc. To implement this method, you should draw up a package of documents, which will include:

- statute on the authorized capital,

- act on the transfer of property to the balance sheet of the enterprise,

- property appraisal protocol.

On the procedure for making a contribution to the authorized capital

First of all, the property to be contributed to the authorized capital must be assessed. This procedure is carried out by the Board of Directors (in the case of Joint-stock company) together with an involved independent appraiser. Moreover, he has no right to establish a higher price than the announced one.

In the case of the establishment of a Limited Liability Company (LLC), the cost of the minimum allowable authorized capital is ten thousand rubles.

There is no need to pay the entire amount at the establishment. It is enough to deposit five thousand at once, and then, within a year, the remaining funds.

If the founder is a single person, his sole decision is sufficient when drawing up a protocol on the value of the property. If the estimated cost is more than twenty thousand rubles, then, before depositing the authorized capital with property, the latter is assessed with the invitation of a professional appraiser.

Samples of all required documents- typical, but can be adjusted to suit your own needs and in agreement with lawyers.

Legal requirements

The property is transferred to the balance sheet of the established enterprise with the drawing up of an act of transfer. It is signed by each of the founders.

A prerequisite is the inclusion in the relevant sections of the Charter and the Memorandum of Association (if the number of founders is more than one) the very possibility of contributing the authorized capital by property. As well as restrictions on types of property.

The property contribution made to the authorized capital is not, according to the law, a gratuitous transfer. The contributing party (investor) receives the rights to receive a certain part of the profits earned by the Company, as well as a certain part of the property in the event of liquidation.