Whether you use the electronic payment system (Bank-Client system), 1C Enterprise, or create a payment card in any other program, you have to take into account quite a lot of data. Let's break it down into parts and deal with each one. The author offers you a detailed description of the procedure for filling out a payment order. Even a person who is not a happy owner of accounting programs can fill it out on their own. This is what a payment order looks like (see Example 1). Each field that should be taken into account when filling it out has a corresponding number in brackets.

The data that is entered into the payment order is called the general word “details”.

Regardless of who you send the payment to (the tax office or the supplier of the goods), you must fill in field No. 2. This number is always the same and unchanged (0401060). And it means the number of the unified form of payment order, which is established by the Central Bank of the Russian Federation.

In field No. 3 “Payment order number” the payment order number is indicated in numbers. From the beginning of the year, numbering begins again.

In field No. 4 “Date of payment order” the day, month, year are indicated. It is filled out in the format DD.MM.YYYY. For example, 02/06/2007. The word “year” is not written, and there is no dot after the year number.

Field No. 5 “Type of payment” is filled in only if an “electronic” payment is made, that is, you send a payment through the “Bank-Client” system. This is what it says here: “electronically”. If you yourself are going to take the payment order to the bank, then you don’t need to write anything.

In field No. 6 “Amount in words”, from the beginning of the line with a capital letter, indicate the payment amount in words in rubles and kopecks. At the same time, the words “rubles”, “ruble”, “ruble”, “kopecks”, “kopek” are not abbreviated. Rubles are written in words, and kopecks in numbers. If the payment amount is expressed only in rubles, then kopecks may not be indicated.

In field No. 7 “Amount”, enter the payment amount in numbers, rubles are separated from kopecks by a dash sign “-”. If the amount is expressed in numbers in whole rubles, then kopecks may not be indicated. In this case, the payment amount and the equal sign “=” are shown, while in the “Amount in words” field the payment amount is entered in whole rubles, without mentioning kopecks.

See an example of completed payments below.

The author recommends that you choose one of the methods and use it. Otherwise, you can get confused about what to write and when. It will be unpleasant when you urgently need to transfer money, and the bank refuses to accept your payment order due to an error.

In field No. 60 “TIN” the taxpayer identification number is indicated.

In field No. 102 “KPP” - the reason for registration assigned to the organization by the tax inspectorate at the place of registration. Let us remind you that an individual entrepreneur and ordinary individuals do not have a cash register. If the payment goes to them or from them, then “0” is placed in this field.

In field No. 8 “Payer”, indicate the person who sends the payment (pays). For example, if an entrepreneur does this, then, accordingly, he indicates himself (full full name and next to them in brackets - individual entrepreneur (order of the Ministry of Finance of the Russian Federation of November 24, 2004 No. 106n)). However, in practice it is necessary to be guided by the requirements of the bank. The bank may require that the payer indicate himself in accordance with how he named himself on the bank card when he certified his signature at the bank.

In the example under consideration, this may look, for example, as individual entrepreneur Svetikova Svetlana Pavlovna or individual entrepreneur Svetikova Svetlana Pavlovna. The bank may not allow your payment due to such an error. Moreover, if you send a payment to an individual entrepreneur, then it does not matter how it is written in the payment order. For legal entities, the abbreviations “ZAO” and “LLC” are accepted. But always look at how counterparties call themselves in the agreement or invoice that is issued to you for payment. If there is an error in the name of the recipient, then the partners may not receive the money.

If you still made a mistake, then you urgently need to send a letter to the bank, where you need to clarify the name of the recipient and indicate all the details of the payment order. If you were late with the clarification letter, then the money will be returned to your account. The only trouble will be that the money will “let slip” for about a week.

In field No. 9 “Account. No." indicates the payer's current account number.

In field 10 “Payer's bank” - the full name of the payer's bank indicating the city of its location.

In field No. 11 “BIC” is the bank identification code (BIC) of the payer’s bank.

In field No. 12 “Account. No. - number of the correspondent account of the payer’s bank, opened by a credit institution in an institution of the Bank of Russia.

In field No. 13 “Recipient's bank” - the full name of the recipient's bank indicating the city of its location.

In field No. 14 “BIC” is the bank identification code (BIC) of the recipient’s bank.

In field No. 15 “Account. No. - the number of the correspondent account of the recipient's bank, opened by a credit institution in an institution of the Bank of Russia.

In field No. 61 “TIN” the recipient’s identification number is indicated.

In field No. 103 “KPP” - the code of the reason for registering the recipient of funds.

In field No. 16 “Recipient” - the name of the recipient organization or full name. individual.

In field No. 17 “Account. No. indicates the recipient's current account number.

In field No. 18 “Type of op.” the type of operation is indicated. “01” is the bank code for payment by payment order.

In field No. 19 “Payment deadline.” the payment deadline is indicated.

In field No. 20 “Name of pl.” The code purpose of the payment must be indicated.

This column is not filled in until instructed by the Bank of Russia.

In field No. 21 “Design.plate.” The order of payment is indicated.

The sequence numbering is as follows:

Sequence 1. Write-offs are carried out according to executive documents providing for the transfer or issuance of funds from the account to satisfy claims for compensation for harm caused to life and health, as well as for the collection of alimony.

Sequence 2. Write-offs are made according to executive documents providing for the transfer or issuance of funds for settlements for the payment of severance pay and wages with persons working under an employment agreement (contract), remuneration under copyright agreements.

Sequence 3. The number 3 is not used.

Sequence 4. According to this priority, write-offs are made on payment documents providing for payments to the budget and extra-budgetary funds. These are taxes, fines, penalties, state duties.

Sequence 5. Intended for write-off according to executive documents providing for the satisfaction of other monetary claims.

Sequence 6. Write-offs are made for other payment documents in calendar order. These include payments to suppliers.

Field 22 “Code” is not filled in until instructed by the Bank of Russia.

Field 23 “Res.field” is reserved.

Field No. 24 “Purpose of payment” reflects the content of the transaction carried out by the payment order.

Example 3

Collapse Show

CJSC "Ideas for the Home" transfers by payment order the payment to the counterparty for performing work under contract No. 55 dated January 25, 2007. The payment is 50,000 rubles, including VAT - 7,627.12 rubles. The company fills out the payment form as follows:

Let's continue the conversation about field 24 “Payment purpose”. The following points can be reflected here:

- name of goods, works, services (for example, for office equipment, for transportation services);

- numbers, names and dates of documents justifying the operation of transferring funds (agreements, invoices, work acceptance certificates);

- deadline for transferring funds.

If payment is made before receipt of goods or provision of services, then you write: "prepayment".

Before the work is completed - "advance payment".

For the service provided - "services provided".

For the work done - "at final settlement".

In connection with changes in any conditions (scope of delivery, work, services; errors in calculations; changes in prices) - "additional fee".

In the latter case, it is necessary to indicate that this payment is an additional payment to the previously transferred payment, for example, an additional payment under supply agreement No. 120 dated March 13, 2007.

Here you must also indicate (see Example 3) the amount of VAT in the total payment amount. If the one who receives the payment works without VAT, then it should be written: “VAT not subject to” or: “Without VAT.”

In field No. 43 a stamp is placed in the strictly designated place. Entrepreneurs who carry out their activities without a seal should write in pen in the space reserved for the seal: “b/p”.

Field No. 44 “Signatures” is signed by a person who has the right to sign, and this right is secured by a sample of his signature certified by the bank on the bank card. There may be two signatures. If there is a chief accountant on staff, then, accordingly, both signatures must be certified on the bank card. You can make the option of two equivalent signatures. That is, two people have the right of first signature, but one of the signatures is placed on the payment order.

The stamp and signature are placed on the first copy of the payment order. There can be two copies in total (usually three or more). All copies of payment slips are handed over to the bank operator. On one of them, the operator puts the bank’s mark in field 45. At the same time, this copy of the order bears the stamp of the bank and the signature of the operator who accepted the order for execution.

Fields No. 62 and No. 71 are also filled out in the bank. In field 62, the bank operator enters the date of submission of the payment order to the bank. And in field 71 - the date of debiting funds from the client’s account for this payment order.

Field No. 101, located in the upper right corner of the payment order, and fields 104-110 are filled in in case of transfer of taxes, fees and other obligatory payments to the Russian budget system.

Well, we’ve dealt with simple payments, now let’s look at a payment order with the transfer of taxes.

Transfer of tax payments

When a taxpayer transfers payments to the budget system of the Russian Federation, field No. 101 is filled in. It indicates the status of the payer. We are primarily interested in status 01 - taxpayer (payer of fees) - legal entity. This is what should be indicated when transferring taxes, fees and other obligatory payments.

In general, there are other statuses:

- 02 - tax agent;

- 03 - collector of taxes and fees;

- 04 - tax agent;

- 05 - bailiff service of the Ministry of Justice;

- 06 - participant in foreign economic activity;

- 07 - customs authority;

- 08 - payer of other obligatory payments, making transfers of payments to accounts for accounting income and budget funds of all levels of the budget system of Russia;

- 09 - individual entrepreneur;

- 10 - taxpayer (payer of fees) - private notary;

- 11 - taxpayer (payer of fees) - lawyer who established a law office;

- 12 - taxpayer (payer of fees) - head of a peasant (farm) enterprise;

- 13 - taxpayer (payer of fees) - another individual - bank client (account holder);

- 14 - taxpayer making payments to individuals (subclause 1, clause 1, article 235 of the Tax Code of the Russian Federation);

- 15 - a credit organization that has issued a settlement document for the total amount for the transfer of taxes, fees and other payments to the budget system of the Russian Federation, paid by individuals without opening a bank account.

When transferring taxes, the fields discussed above are filled in similarly. We now turn our attention to fields from 104 to 110.

Only one tax/fee can be transferred with one payment order.

So, in field No. 104 “Budget classification code” (BCC) is indicated in accordance with the classification of budget income of the Russian Federation, has 20 characters.

Field No. 105 “OKATO code” indicates the code of the municipality in whose territory funds from paying taxes / fees are mobilized. Filled out in accordance with the All-Russian Classifier of Objects of Administrative-Territorial Division. You can also find out what OKATO your tax office has on the website www.nalog.ru or simply at your tax office at the information stands.

In field No. 106 “Basis of payment” there are letter indicators. One of them is indicated in the payment order.

If you enter “0” in this field, then the tax authority has the right to independently attribute the payment to one of the listed grounds, guided by the legislation on taxes and fees.

Field No. 107 “Tax period” is used to indicate the frequency of payment of the tax / fee or the specific date for payment of the tax / fee established by tax legislation. The indicator contains ten characters along with dots.

For example, the deadline for paying the annual tax under the simplified taxation system for 2007 is GD.00.2007. It is this value that will appear in field 107. If payments are quarterly - for the first quarter of 2008 - KV.01.2008. Payroll taxes must be remitted by the 15th of the month following the month of payment. Thus, for December 2007, “salary” taxes are until January 15, 2008, and personal income tax is transferred on the day the salary is paid.

Field No. 108 “Document number” indicates the number of the document on the basis of which the payment is made. Depends on the basis of the payment. The “No” sign is not affixed. If a current payment or voluntary repayment of debt is made, then “0” is entered in this field.

Field No. 109 “Document date” indicates the date of the document on the basis of which the payment is made. Just as in the previous case, it consists of ten characters (including dividing points between the day, month and year), but contains only numbers. When transferring current tax payments or voluntarily repaying debts, they usually set the date for signing the declaration. If the payment comes after a tax audit, then the date of the document with the requirement to repay the arrears is written. And in field 108 the number of this requirement will be indicated.

Field No. 110 “Payment Type” has two alphabetic characters.

If “0” is indicated in this field, then tax authorities have the right to independently classify the payment as one of the listed types of payment (tax, penalty, interest or fine), guided by the legislation on taxes and fees.

In field No. 24 “Purpose of payment” the necessary additional information is indicated. For example, if tax is transferred to the Pension Fund of the Russian Federation for its insurance part, then it should be written: “PFR insurance part, your number in the Pension Fund of the Russian Federation as an employer and the period for which the payment is made.”

Example 4

Collapse Show

CJSC Romulus transfers by payment order the Unified Social Tax to the pension fund for the insurance part of the pension for January 2008.

BCC of this tax is 18210202010061000160.

The CJSC is registered with the Federal Tax Service No. 5 in Moscow.

OKATO code - 45286560000.

Since the entrepreneur independently pays the calculated current tax, this means that the “Base of payment” is TP.

Payment of tax for January, therefore, “Tax period” - MS.01.2008.

The payment is current, so the document number is “0” and the document date will be “0”, since declarations are signed only once a quarter, and the tax is paid only for the first month of the first quarter.

The indicator “Payment type” has the value NS.

The payment order of Romulus CJSC will look like this.

A payment order is an order to the bank to transfer the appropriate amounts to suppliers, financial authorities, and other organizations. The accountant prints it “as a carbon copy” in the required number of copies (from 3 to 5, depending on which branch of the bank the current account is located).

A payment order is accepted by the bank from the payer for execution only if there are funds in the current account, unless otherwise agreed between the bank and the account owner. By agreement of the parties, payment orders can be urgent, early or deferred. Urgent payments are made: before the shipment of the goods - an advance payment, after the shipment of the goods - by direct acceptance of the goods, for large transactions - partial payments. Early and deferred payments can be made within the framework of contractual relations without prejudice to the financial position of the contracting parties.

It indicates the details of the payer and his bank, the recipient and his bank, including TIN, BIC, amount and purpose of payment. The bank employee accepts the payment order for execution, puts a stamp on the last copy and returns it to the accountant to reflect this operation in accounting. The printed payment order is valid for ten days.

The TIN is assigned to the bodies of the State Tax Service of the Russian Federation when taxpayers are registered with the tax authority and is indicated in the payment order in all cases when it is assigned to the payer of funds.

The BIC is indicated for divisions of the settlement network of the Bank of Russia, credit institutions and those branches of credit institutions to which it is assigned, in accordance with the “BIC of the Russian Federation Directory”.

The account numbers of the payer and recipient of funds, as well as the bank account numbers of the payer and recipient for which settlement transactions are carried out, are entered in the appropriate fields of the payment order.

If the payer or recipient is a credit institution, the name of the credit institution is indicated in the fields “Payer” or “Recipient”; in the fields “Bank”

payer” or “recipient’s bank”, respectively, name

the credit institution is indicated again. The value “Type of payment” is indicated in words: “mail”, “telegraph”, “electronically”.

The payer is the bank in which the company's current account is opened; in the same part the name of the enterprise and the number of its current account are indicated.

Below we indicate the code that is assigned to our bank in the Central Bank of the Russian Federation, and in the “debit” column - the code of the bank’s current account with the Central Bank of the Russian Federation.

The amount is printed in capital letters. Its digital value is repeated in the upper right corner.

At the bottom, the purpose of the payment is indicated in detail, the signature of the fund manager and the chief accountant and the seal of the enterprise are affixed.

2.3 Procedure for receiving cash from the bank.

A business receives cash from a bank through a teller using a cash check written in its name.

In accordance with the Regulations on Accounting and Reporting in the Russian Federation, at enterprises that do not have a cashier on staff, the cashier’s duties can be performed by the chief accountant or another employee by written order of the head of the enterprise.

Checks are kept in a special checkbook. To receive a checkbook, you must fill out the appropriate application, which indicates the last name, first name and patronymic of the cashier and provides a sample of his signature. The application is signed by the manager and chief accountant and certified by the seal of the enterprise. According to this statement, the cashier receives a checkbook for 25 or 50 checks. To withdraw cash from your bank account, the accountant fills out a cash check, signs it with your manager, and hands it to the teller. The cashier pre-orders the required amount with a supporting document for recording cash transactions in accounting registers.

2.4. Procedure for depositing cash at the bank

Cash received from the current account to the cash desk,

are spent strictly for their intended purpose (the purposes for which the money was received are indicated on the back of the cash receipt). The unspent balance is handed over to the cashier. For example, wages not received on time must be returned to the current account within three days. Money received at the cash desk as a contribution to the authorized capital, proceeds from the sale of products in cash are deposited into the current account

The transfer of money to the current account is formalized by a cash receipt order.

At the bank, the cashier who deposits the money fills out an “Announcement for Cash Deposits.” The “Announcement” form can be obtained from the bank operator.

It consists of three parts. The top part remains in the jar,

The middle part (receipt) is given to the cashier. The lower part of the advertisement (order) is also returned to the cashier, but only after the bank has carried out the corresponding operation and together with the bank statement.

Each of the three parts is marked with: the date from whom the money was received, the recipient's bank and the recipient, the purpose of the contribution. In the upper right corner of the first and second parts we put our current account number and the amount in numbers. The same amount is written in words in the following order. The entry must begin close to the beginning of the field allocated for it with a capital letter. The remaining spaces on the field should be crossed out with a horizontal line.

The third part is filled out a little differently. In the order you need to indicate the code of the recipient bank and the amount of the loan (in our current account this amount will be debited, and in the bank - as a loan).

In 2017, changes were again introduced in the design and preparation of payment documents for the transfer of taxes and insurance premiums. Below are the rules for filling out the fields of a new payment order - payment slip - for transferring personal income tax, UTII, simplified taxation system and insurance contributions to the Federal Tax Service of the Russian Federation and the Social Insurance Fund. As well as the use of cash register systems in non-cash payments.

NEW PAYMENT ORDER - PAYMENT in 2019

When paying taxes and insurance premiums to the budget, use standard payment order forms. The form and fields of the payment order, numbers and names of its fields are given in Appendix 3 to the regulation approved by the Bank of Russia dated June 19, 2012 No. 383-P.

What kind of estimate item should be filled out in the payment slip? The rules for filling out new payment orders in 2019 when transferring tax payments to the budget were approved by order of the Russian Ministry of Finance dated November 12, 2013. No. 107n. These rules apply to everyone who transfers payments to the budget system of the Russian Federation:

- payers of taxes, fees and insurance premiums;

- tax agents;

- payers of customs and other payments to the budget.

A cash register is required for all non-cash payments.

The requirement for which payment methods must be used is changed. The law introduced the concept of “non-cash payment procedure”. Before the amendments, it required the use of cash register systems only for cash payments and non-cash payments using electronic means of payment (EPP). The definition of ESP is in the Law of June 27, 2011 No. 161-FZ “On the National Payment System”. This is for example:

- bank card;

- any electronic wallets;

- online banking, etc.

CCP for non-cash payments: what has changed

WasCash register systems are used when accepting or paying funds using cash and (or) electronic means of payment for goods sold, work performed, services provided...

It becameCash register systems are used when accepting (receiving) and paying funds in cash and (or) by bank transfer for goods, work, services...

Since July 3, 2018, the law requires the use of cash register systems for any method of non-cash payment. For example, when paying by receipt or payment order through a bank. But additional checks will need to be punched only from July 1, 2019. Non-cash payments, except for electronic means, were exempted from cash register until July 1, 2019 (Clause 4, Article 4 of Law No. 192-FZ dated 07/03/2018).

Answers to frequently asked questionsIs it now necessary to use cash register systems for non-cash payments with individuals?

Yes need. From July 1, 2018, it is necessary to use cash register systems, but only when making payments using electronic means of payment. For example, when paying through electronic wallets and online banking. For new non-cash payment methods there is a deferment until July 1, 2019. That is, when paying receipts and payment orders through an operator at a bank, cash register will need to be used only from July 1, 2019. This follows from paragraph 1 of Article 1.2, paragraph 21 of Article 1.1 of the Law of May 22, 2003 No. 54-FZ, paragraph 4 of Article 4 of the Law of July 3, 2018 No. 192-FZ.

Is it necessary to use cash register systems for non-cash payments with organizations and individual entrepreneurs?

No, for non-cash payments with organizations and individual entrepreneurs, it is not necessary to use cash register systems in principle. An exception is settlements with the presentation of an electronic means of payment. For example, when making payments using a card. If payments are made through the Client-Bank system, then cash register is not required. This is a non-cash payment without presenting an electronic means of payment. This is stated in the Law of May 22, 2003 No. 54-FZ.

to menu

From June 2018, new rules for non-cash payments

These changes apply to all organizations and entrepreneurs.

From June 1, 2018, the rules for non-cash payments are changing (Law No. 212-FZ dated July 26, 2017). Previously, the bank could ask the client to clarify the payment order. The bank only rejected the payment if the customer did not respond. Now, after the bank has accepted the payment order, it must:

- make sure that the payer has the right to dispose of the money;

- check whether the payment meets the established requirements;

- find out whether there is enough money in the account for payment;

- carry out other procedures according to bank instructions.

According to the new rules, the bank cannot ask the client to clarify the contents of the payment. This means that from June 1, 2018, the bank formally has the right to refuse due to any error in the payment order (). The error can be corrected only if there is an internal instruction of the bank that allows you to request clarification from the client. For late payment due to inaccuracies in the payment, counterparties will have to pay a penalty or legal interest, and the Federal Tax Service will have to pay a penalty.

New rules for filling out payment orders for personal income tax from August 1, 2016

In field 110 When transferring taxes from 2015, you will not need to fill out field “110” and indicate the type of payment (penalties, interest, fine, debt). Tax authorities and funds can identify the type of payment by KBK.

Payment amount in words field 6 indicated only in paper payments; in the electronic version, the amount is not indicated in words.

In field 21 " " you need to write a number 5 , and before there were 3.

Note: Changes have been made to . The bank should not refuse to accept a paper payment order if the “Payment order” detail is filled in incorrectly. If your servicing bank refused to execute the payment for this reason, you can report this to the Central Bank. (Letter of the Ministry of Finance dated October 4, 2017 No. 05-09-06/64623)

In field 22 props" Code" instructions for transfer of funds indicate a unique accrual identifier WIN.

The value 0 is written instead of UIN if you transfer the payment yourself and not on demand.The requirement to fill in the “Code” details applies to orders for the transfer of funds, the forms of which are established by Bank of Russia Regulation No. 383-P.

Note: . It is explained what UIN value to add to the CODE detail in field 22 of the payment order.

to menu

Paying taxes for third parties: how to fill out a payment form

From November 30, 2016, it became possible to transfer taxes to the budget for another person (both legal and physical). The Federal Tax Service said.

Legal entities can transfer taxes from their account to other organizations, and managers have the right to pay off the company's tax obligations from their own funds. This is also true for fees, penalties, fines, insurance premiums and applies to fee payers, tax agents and the responsible participant in the consolidated group of taxpayers.

Note: The Federal Tax Service of Russia, in a letter dated January 25, 2018 No. ZN-3-22/478@, explained how in such cases it is necessary to fill out the “TIN”, “KPP” and “Payer” fields of payment documents.

In filling out the payment field 24 « Purpose of payment» additional information related to the transfer of funds to the budget and extra-budgetary funds is indicated.

For example, when paying insurance premiums, in this field you can indicate the short name of the extra-budgetary fund (FSS, FFOMS or Pension Fund) and the registration number of the organization.

If tax is transferred, indicate the name of the tax and for what period the payment is made. For example: “Payment of VAT for the first quarter of 2017”, “Payment of income tax for the first quarter of 2017”.

In this case, the total number of characters in the “Purpose of payment” field should not exceed 210 characters (Appendix 11 to the regulation approved by the Bank of Russia dated June 19, 2012 No. 383-P).

For your information

When transferring insurance premiums for current periods, in the “Purpose of payment” field, be sure to indicate the month for which the premiums are paid. Otherwise, if an organization has an overdue debt, the tax office will use the funds received to pay off this arrears.

If the payment order for the transfer of insurance premiums does not allow you to determine the purpose of the payment and the period for which the payment is made, then the fund will first credit the contributions to repay the debt that was formed earlier. And only after that the remaining amount will be counted towards current payments.

Individual Entrepreneurs (IP) When filling out a payment order, new payment orders for 2019, you must also indicate the address of your registration or place of residence, enclosed in the symbols “//”.

In field 8 on the payment form, the entrepreneur fills out the last name, first name, patronymic and in brackets - “IP”, as well as the registration address at the place of residence or the address at the place of stay (if there is no place of residence). Before and after the address information you must put a “//” sign.

Example: Petrov Ivan Petrovich (IP) //Moscow, Petrovka 38, room 35//

Place the checkpoint and OKTMO of the separate division for whose employees the company transfers personal income tax

A letter from the Federal Treasury designated the period from 01/01/2014 to 03/31/2014 as a transition period during which it is possible, but not necessary, to indicate the UIN. From April 1, 2014, the procedure for specifying identifiers will be mandatory.

Number of characters in fields 8 and 16: “payer” and “recipient” should not be more than 160.

Note: See letter of the Pension Fund of Russia No. AD-03-26/19355 dated 12/05/13

The rules for processing all other payments, except for taxes, contributions and payment for municipal and government services, remain the same.

A taxpayer who learns that due to an error made in a payment order, the tax is not reflected in the personal account, must take certain actions. Read the topic "" about them.

Note: A section has been opened for organizations and individual entrepreneurs on all taxes and fees. Come in any time. Download completed examples of payment slips 2019.

to menu

Details for filling out payment slips for taxes and contributions will change in 26 regions

From February 4, 2019, you need to be more careful when filling out payment slips for taxes, fees, fines and other payments. The Federal Tax Service of Russia announced that in a number of regions the number of the federal treasury department will change. The table of correspondence between old and new bank accounts is given in the letter of the Federal Tax Service dated December 28, 2018 No. KCH-4-8/25936@.

New UFK numbers will need to be indicated on payments as of February 4. At the same time, the Central Bank established a “transition” period. Thus, when filling out payment slips, two bank accounts (old and new) are allowed to function until April 29, 2019. After this date, payers will only need to provide new details (letter of the Federal Treasury dated December 13, 2018 No. 05-04-09/27053).

ADDITIONAL LINKS on the topic

- Examples of FILLING PAYMENTS TO THE TAX OFFICE

The rules for filling out payment orders when transferring payments to the budget were approved by Order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n. They apply to everyone who makes payments: payers of taxes, fees and insurance premiums.

Rules are provided for specifying information in details 104 - 110, “Code” and “Purpose of payment” when drawing up orders for the transfer of funds for the payment of taxes, insurance fees and other payments to the budget system of the Russian Federation.

Rules are given for indicating information identifying the person or body that issued the order for the transfer of funds for payment of payments to the budget system of the Russian Federation. Code in field 101 of the payment card.

A taxpayer who learns that due to an error made in a payment order, the tax is not reflected in the personal account must take the following actions...

What do sample payment orders look like in 2017? What has changed is new requirements for filling out payment orders.

Samples are presented for payment orders relating to personal income tax, simplified tax system, and other contributions paid to state funds

What does the 2017 payment order consist of?

A payment order created to generate and reflect the amount required for the payment of taxes, fees and contributions for the purpose of insuring employees of an enterprise is carried out on form 0401060. Each field has a separate number. It is necessary to fill out the document in accordance with the KBK for paying tax deductions and making contributions, which is carried out in 2017.

At the same time, in 2017 the following features should be taken into account:

It is impossible to apply the BCCs in force in 2016; for example, the BCCs for contributions to the Pension Fund are outdated.

The data on line 110 in the PDF has also changed.

In 2017, the information to be filled in regarding contributions and tax amounts is the same:

1. Paragraph 1 describes the name of the organization.

3. In column 3, enter the payment number, which is written not in words, but in numbers.

4. Clause 4 consists of the date the notification was completed. Here you need to follow these rules:

if the document is submitted on paper, the full date is entered, following the format DD.MM.YYYY;

The electronic version involves recording the date in the format of the credit institution. The day is indicated by 2 digits, the month by two, and the year by four.

5. In paragraph 5, record one of the values: “urgent”, “by telegraph”, “by mail” or another indicator determined by the bank. You can leave the column empty if the bank allows it.

6. In paragraph 6, write the payment amount. In this case, rubles are written in words, and kopecks are listed in numbers. Rubles and kopecks are not reduced or rounded. If the amount to be paid is a whole amount and does not have small change, then pennies separated by commas may not be recorded. In the “Amount” line, the amount is set, followed by the equal sign “=”.

7. Clause 7 contains the amount to be paid, determined in numbers. Rubles are separated from change using a dash sign “–”. If the number is an integer, then an equal sign “=” is placed after it.

8. Paragraph “8” contains the name of the payer; if it is a legal entity, you need to write the name in full, without abbreviations or abbreviations.

9. In paragraph 9, enter the number of the payer’s account registered with the banking institution.

11. Point 11 shows the bank code identifying the institution where the payer of taxes and contributions is served.

12. Paragraph 12 consists of the correspondent account number of the taxpayer’s bank.

13. Clause 13 determines the bank that will receive the transferred funds. Since 2014, the names of Bank of Russia branches have changed, so check this issue on the official website of the financial institution.

14. Point 14 consists of the bank identification code of the institution receiving the money.

15. In column 15 you should write down the number of the corresponding bank account to which contributions are transferred.

16. Line 16 contains the full or abbreviated name of the enterprise receiving the funds. If this is an individual entrepreneur, write down the full last name, first name and patronymic, as well as legal status. If this is not an individual entrepreneur, it is enough to indicate the citizen’s full name.

17. Column 17 records the account number of the financial institution receiving the money.

18. Props 18 always contains the encryption “01”.

19. As for detail 19, nothing is recorded here unless the bank makes a different decision.

20. 20 props also remain empty.

21. Line 21 requires determining the order of the amount to be paid in a figure corresponding to legislative documents.

22. Requisite 22 presupposes a classifier code for the amount to be paid, whether it be contributions or tax deductions. The code can consist of either 20 or 25 digits. The details exist if they are assigned by the recipient of the money and are known to the taxpayer. If an entrepreneur independently calculates how much money he should transfer, there is no need to use a unique identifier. The institution receiving the money determines payments based on the numbering of TIN, KPP, KBK, OKATO. Therefore, we indicate the code “0” in the line. The request of a credit institution is considered illegal if, when recording the TIN, you need to additionally write information about the code.

23. Leave field 23 blank.

24. In field 24, describe the purposes for which the payment is made and its purpose. It is also necessary to indicate the name of goods, works, services, numbering and numbers used in documents according to which payment is assigned. These can be agreements, acts, invoices for goods.

25. Requisite 43 includes affixing the IP seal.

26. Field 44 consists of the signature of an authorized employee of the organization, manager or corresponding authorized representative. To avoid misunderstandings, the authorized representative must be entered on the bank card.

27. Line 45 contains a stamp; if the document is certified by an authorized person, his signature is sufficient.

28. Requisite 60 records the taxpayer’s TIN, if available. Also, those who recorded SNILS in line 108 or the identifier in field 22 can enter information in this line.

29. The recipient’s TIN is determined in detail 61.

30. In line 62, the employee of the banking institution enters the date of submission of the notification to the financial institution related to the payer.

31. Field 71 contains the date when money is debited from the taxpayer’s account.

32. Field 101 records the payer status. If the organization is a legal entity, write down 01. If you are a tax agent, enter 02. Coding 14 applies to payers who settle obligations with individuals. This is just a small list of statuses; a more complete one can be found in Appendix 5 to the order of the Ministry of Finance of Russia, which was issued in November 2013 and registered in the register under number 107n.

33. Field 102 consists of the checkpoint of the payer of contributions and taxes. The combination includes 9 digits, the first of which are zeros.

34. Field 103 – checkpoint of the recipient of funds.

35. Line 104 indicates the BCC indicator, consisting of 20 consecutive digits.

36. Props 105 shows the OKTMO code - 8 or 11 digits, they can be recorded in the tax return.

37. In detail 106, when making customs and tax payments, record the basis of the payment. TP is indicated if the payment concerns the current reporting period (year). ZD means the voluntary contribution of money for obligations occurring in past reporting periods, if there are no requirements from the tax office for payment.

Where can I get a complete list of possible values? In paragraph 7 of Appendix 2 and paragraph 7 of Appendix 3 to the order of the Ministry of Finance of Russia, issued in 2013.

If other deductions are made or it is impossible to record a specific indicator, write “0”.

38. Requisite 107 is filled in in accordance with the purpose of the payment:

if taxes are paid, the tax period is fixed, for example, MS 02.2014;

if customs payments are made, the identification code of the customs unit is indicated;

you need to deposit money in relation to other contributions - write “0”.

39. Payment of tax contributions involves entering a paper number, which serves as the basis for the payment.

40. What data is recorded in field 109?

if tax revenues and deductions to the customs authorities are to be paid, determine the date of the paper that is the basis for the payment, pay attention to the presence of 10 digits in the encoding (the full list of indicators can be found in paragraph 10 of Appendix 2 and paragraph 10 of Appendix 3 to the order of the Ministry of Finance of Russia, registered in November 2013);

if other money is transferred to state budget funds, write “0”.

In field 110 there is no longer a need to fill in the type of deductions.

Features of drawing up line 107 in the payment slip for 2017

Accountants are interested in the subtleties of filling out line 107, located in the payment document in 2017. Detail 107 indicates the tax period when the contribution or tax is paid. If it is not possible to determine the tax period, “0” is entered in column 107.

What components does the tax period indicator consist of and what does it indicate, experts shared:

The 8 digits of the combination differ in their semantic meaning;

2 digits are considered separating digits and are therefore separated by a dot.

The value of detail 107 determines the frequency of payment:

monthly regularity (MS);

quarterly (QW);

semi-annual (PL);

annual (AP).

What do the signs mean?

The first 2 characters indicate the frequency of payment of money.

4-5 characters provide information regarding the month number of the reporting period; if we are talking about quarterly payments, the quarter number is fixed; for semi-annual deductions, the semi-annual number applies. As for the monthly designation, it can be a figure from 01 to 12. The quarter number consists of the values 01–04. The half-year number is recorded as 01–02.

3-6 signs of props 107 are always separated by dots.

Digits 7-10 contain the year in which contributions are paid.

If the payment is made only once a year, then the 4th and 5th digits are represented by “0”.

Samples of how to fill out line 107 in a payment slip for 2017

What might examples of field 107 look like in a payment order for 2017? Examples are presented below:

Tax reporting period in line 107 of the payment document

The tax period is recorded in payment slips in 3 cases:

if payments are made in the current reporting period;

if the reporting person independently discovers erroneously indicated data on the tax return;

upon voluntary payment of additional tax amounts for the past reporting period, if a requirement has not yet been received from the tax authority regarding the need to pay fees;

The value of the tax period for which additional funds are deposited or paid is recorded.

If any type of debt that has arisen is being repaid, be it an installment debt, deferred or restructured, and a bankruptcy case is being considered for an enterprise with debts or an outstanding loan, it is necessary to record a specific number indicating the day on which the amount of money was paid. The payment deadline is indicated as follows:

TR – fixes the payment period, which is determined in the notification received from the tax authority to pay the required amount;

RS – the number when part of the installment debt in relation to tax contributions is paid, taking into account the installment schedule;

OT – focuses on the end date of the deferment period.

RT is the date when a certain share of the restructured debt is paid, which corresponds to the schedule.

PB is the number when the procedure comes to an end, which occurs when the organization goes bankrupt.

PR – the number when the suspension of debt collection ends.

In – fixes the date of payment of the share of the investment loan for taxes.

If the payment intends to repay the debt and is carried out in accordance with the audit report or according to the writ of execution, “0” is recorded in the value of the tax reporting period. If the tax amount is transferred before the due date, then the head of the enterprise fixes the future tax period in which the payment of fees and tax deductions is planned.

The order of deductions in the 2017 payment order

What order the payer follows is reflected in the payment slip, namely in column 21. What is the order of deducted amounts? This is the sequence of money debits that a financial institution follows when processing requests from a client. The issue of monitoring the queue is settled by the bank, but the accountant should not completely rely on outsiders; oversee this process yourself.

In each payment order, in field 21, write down the order from 1 to 5. To which order can current deductions be attributed? No less than the fifth stage, because they are carried out on a voluntary basis. As for payment orders from tax authorities and control authorities, they are classified as the third priority. That is, in field 21 you need to write 3.

Current earnings accrued to the organization's employees are also a third-priority payment. Experts spoke in more detail about the order of payments:

The first priority is assigned to payments made under writs of execution that provide for payment for compensation for damage that resulted in deterioration of health and life. This also includes the transfer of money for collection of alimony payments.

Secondly, payments related to severance pay and salaries to former and current employees, and remuneration to authors of intellectual activity are recorded.

The third priority applies to deductions for wages paid to employees. Also, in the third place, it is allowed to write off the debt incurred in relation to the payment of taxes and fees in connection with a notification received from the tax service. Insurance premiums paid on behalf of regulatory and audit authorities also occupy third place.

Other monetary claims are distributed in the fourth order.

The remaining deductions adhere to the calendar queue - the current amounts of deductions that are directly related to taxes and contributions.

Table. Status of payer of contributions and taxes in 2017

Column 101 of the payment order contains information about the status of the payer of funds. The status can be determined based on the information specified in Appendix 5 to the order of the Ministry of Finance, registered under number 107n. We have already talked about the main statuses above, the rest are reflected in the following table:

| Status number (enter in field 101) | The meaning of payer status in 2017 |

| 01 | taxpayer (payer of fees) - legal entity |

| 02 | tax agent |

| 03 | federal postal service organization that drew up an order for the transfer of funds for each payment by an individual |

| 04 | tax authority |

| 05 | Federal Bailiff Service and its territorial bodies |

| 06 | participant in foreign economic activity - legal entity |

| 07 | customs Department |

| 08 | payer - a legal entity (individual entrepreneur, lawyer, notary, head of a farm) that transfers funds to pay insurance premiums and other payments to the budget |

| 09 | taxpayer - individual entrepreneur |

| 10 | taxpayer - notary engaged in private practice |

| 11 | taxpayer - lawyer who established a law office |

| 12 | taxpayer - head of a peasant (farm) enterprise |

| 13 | taxpayer - another individual - bank client (account holder) |

| 14 | taxpayer making payments to individuals |

| 15 | a credit organization (a branch of a credit organization), a payment agent, a federal postal service organization that has drawn up a payment order for the total amount with a register for the transfer of funds accepted from payers - individuals |

| 16 | participant in foreign economic activity - individual |

| 17 | participant in foreign economic activity - individual entrepreneur |

| 18 | a payer of customs duties who is not a declarant, who is obligated by the legislation of the Russian Federation to pay customs duties |

| 19 | organizations and their branches transferring funds withheld from the wages (income) of a debtor - an individual to repay debts on payments to the budget on the basis of an executive document |

| 20 | credit organization (branch of a credit organization), payment agent, drawing up an order for the transfer of funds for each payment by an individual |

| 21 | responsible member of a consolidated group of taxpayers |

| 22 | member of a consolidated group of taxpayers |

| 23 | authorities monitoring the payment of insurance premiums |

| 24 | payer - individual person who transfers funds to pay insurance premiums and other payments to the budget |

| 25 | guarantor banks that have drawn up an order for the transfer of funds to the budget system of the Russian Federation upon the return of value added tax excessively received by the taxpayer (credited to him) in a declarative manner, as well as upon payment of excise taxes calculated on transactions of sale of excisable goods outside the territory of the Russian Federation , and excise taxes on alcohol and (or) excisable alcohol-containing products |

| 26 |

How to fill out field 101 in a payment slip in 2017?

An example of how to correctly fill out all lines of a payment order in 2017 is presented below.

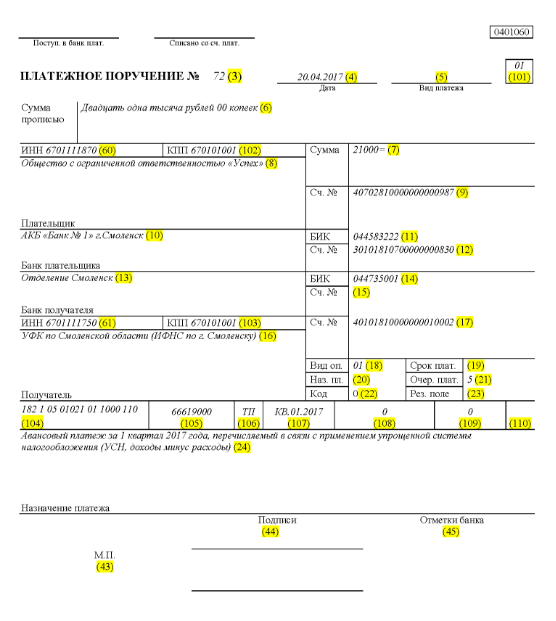

Let’s say a limited liability company with the name “Success” uses a simplified taxation system and operates in the Elninsky district of the Smolensk region. The final indicators for the 1st quarter of 2017 reflected the company’s revenue within the range of 350,000 rubles. There are no preferential tax rates for the income share in the region.

Therefore, the advance amount passing through the simplified tax system, due for the transfer on the completion of the organization’s activities in the 1st quarter of 2017, is:

350,000 * 6% = 21,000 rubles.

This means that the payment order, registered under number 71 on April 14, 2017, will talk about the transfer of money to the tax authority in the form of an advance payment under the simplified tax system for the 1st quarter of 2017 in the amount of 21,000 rubles. An accountant or other accountable person must correctly fill out a payment order for this amount.

So, in accordance with the transfer of tax, the fifth order of payment for tax deductions, insurance premiums and other types of payments is entered in field 21.

In line 101, record 01, because the company transfers tax revenues. In field 104, set the KBK for payment of tax amounts according to the simplified taxation format for income - 18210501011011000110. In line number 105 we write - OKTMO Elninsky district of the Smolensk region - 66619000. In line 106, record TP, and in rook 07 - KV 01.2017, which means movement funds for the 1st quarter of 2017. In section 108 set “0”, in field 109 – also “0”.

Line 22 indicates the LLC’s payment of current tax deductions and contributions, which the enterprise calculated on its own, so we write “0”. The UIN in this case is not recorded. On line 24, provide additional information regarding the transfer of money.

A clear example of what is correct from the point of view of tax accounting and reflection of the cash flow of an enterprise is given below. In a green shade - line numbers of the payment order.

Changes in payment orders from January 1, 2017

The organization pays taxes and insurance premiums, guided by the same filling rules, which come into force on January 1, 2017. The changes affected the filling of fields 107–110.

Another important change is that the BCC relating to insurance premiums has undergone adjustments. New BCCs begin to operate in December 2016.

Sample payment order for insurance payments to state funds from January 1, 2017

Below is a sample of filling out a payment slip regarding the payment of insurance premiums in 2017. In the payment order, you must indicate the details of your tax office, but not the Pension Fund of the Russian Federation or the Social Insurance Fund (as before).

Sample payment slip for advance payment for the 1st quarter of 2017

Sample payment order for an advance payment for the 1st quarter of 2017 under the simplified tax system, income minus expenses

filling rules in a convenient table

The rules for filling out payment orders when transferring payments to the budget in 2017 are determined by Order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n. These rules apply to everyone who transfers payments to the budget system of the Russian Federation:

- payers of taxes, fees and insurance premiums;

- tax agents;

- payers of customs and other payments to the budget;

- third parties who pay taxes or insurance premiums “for others.”

The listed persons must correctly understand how to fill out payment orders in 2017 so that their payments are received as intended and do not have to look for paid taxes or insurance premiums. For these purposes, it recommends paying attention to the table, which contains a breakdown of the fields of the payment order and provides recommendations for drawing up and filling out individual codes. The table already takes into account all changes that came into force on January 1, 2017.

| Payment field | Filling | |

| Payer information | ||

| TIN | Enter the TIN of the payer in the budget (including the tax agent). In this case, the first and second characters cannot immediately be zeros. The field may not be filled in for individuals if they indicated SNILS in field 108 or UIP in field 22. In all other cases, the TIN must be indicated. | |

| checkpoint | Specify the checkpoint of the payer of payments to the budget (including a participant in foreign economic activity, a tax agent). Payers - individuals indicate zero (“0”) in this field. For organizations, the first and second characters cannot be zeros at the same time | |

| Payer | Organizations (separate divisions) indicate their name of the organization | |

| Individual entrepreneurs indicate the surname, first name, patronymic (if any) and in brackets - “IP”, registration address at the place of residence or registration address at the place of residence (if there is no place of residence). Please include a “//” sign before and after the address information. | ||

| Notaries engaged in private practice indicate the last name, first name, patronymic (if any) and in brackets - “notary”, registration address at the place of residence or registration address at the place of residence (if there is no place of residence). Please include a “//” sign before and after the address information. | ||

| Lawyers who have established law offices indicate their last name, first name, patronymic (if any) and in brackets - “lawyer”, registration address at the place of residence or registration address at the place of residence (if there is no place of residence). Please include a “//” sign before and after the address information. | ||

| The heads of peasant (farm) households indicate the last name, first name, patronymic (if any) and in brackets - “peasant farm”, registration address at the place of residence or registration address at the place of residence (if there is no place of residence). Please include a “//” sign before and after the address information. | ||

| Information about the payer (if taxes are paid by a responsible member of a consolidated group of taxpayers) | ||

| TIN | Indicate the TIN of the responsible participant in the consolidated group of taxpayers. The first and second characters cannot be zeros at the same time. | |

| If the payment order is drawn up by a member of a consolidated group, the field shall indicate the TIN of the responsible member of the consolidated group, whose tax obligation is being fulfilled | ||

| checkpoint | Indicate the checkpoint of the responsible participant in the consolidated group of taxpayers. The first and second characters cannot be zeros at the same time. | |

| If the payment order is drawn up by a member of a consolidated group, the field indicates the checkpoint of the responsible member of the consolidated group, whose obligation to pay tax is fulfilled | ||

| Payer | Indicate the name of the responsible participant in the consolidated group of taxpayers. | |

| Field number | Field code | Field code value |

| Payer status | ||

| 101 | 1 | Taxpayer (payer of fees) – legal entity |

| 2 | Tax agent | |

| 6 | Participant in foreign economic activity – legal entity | |

| 8 | An organization (individual entrepreneur) that transfers other obligatory payments to the budget | |

| 9 | Taxpayer (payer of fees) – individual entrepreneur | |

| 10 | Taxpayer (payer of fees) – notary engaged in private practice | |

| 11 | Taxpayer (payer of fees) – a lawyer who has established a law office | |

| 12 | Taxpayer (payer of fees) – head of a peasant (farm) enterprise | |

| 13 | Taxpayer (payer of fees) - another individual - bank client (account holder) | |

| 14 | Taxpayer making payments to individuals | |

| 16 | Participant in foreign economic activity – individual | |

| 17 | Participant in foreign economic activity - individual entrepreneur | |

| 18 | A payer of customs duties who is not a declarant, who is obligated by Russian legislation to pay customs duties | |

| 19 | Organizations and their branches that withheld funds from the salary (income) of a debtor - an individual to repay debts on payments to the budget on the basis of a writ of execution | |

| 21 | Responsible participant of a consolidated group of taxpayers | |

| 22 | Member of a consolidated group of taxpayers | |

| 24 | Payer – an individual who transfers other obligatory payments to the budget | |

| 26 | Founders (participants) of the debtor, owners of the property of the debtor - a unitary enterprise or third parties who have drawn up an order for the transfer of funds to repay claims against the debtor for the payment of mandatory payments included in the register of creditors' claims during the procedures applied in a bankruptcy case | |

| 27 | Credit organizations (branches of credit organizations) that have drawn up an order for the transfer of funds transferred from the budget system, not credited to the recipient and subject to return to the budget system | |

| 28 | Legal or authorized representative of the taxpayer | |

| 29 | Other organizations | |

| 30 | Other individuals | |

| KBK | ||

| 104 | Budget classification code (20 digits) | |

| OKTMO | ||

| 105 | In the payment order, the organization must indicate OKTMO in accordance with the All-Russian Classifier, approved by order of Rosstandart dated June 14, 2013 No. 159-ST (8 digits) | |

| Basis of payment | ||

| 106 | 0 | Contributions for injuries |

| TP | Tax payments (insurance contributions) of the current year | |

| ZD | Voluntary repayment of debts for expired tax periods in the absence of a requirement from the tax inspectorate to pay taxes (fees) | |

| TR | Repayment of debt at the request of the tax inspectorate | |

| RS | Repayment of overdue debt | |

| FROM | Repayment of deferred debt | |

| RT | Repayment of restructured debt | |

| VU | Repayment of deferred debt due to the introduction of external management | |

| ETC | Repayment of debt suspended for collection | |

| AP | Repayment of debt according to the inspection report | |

| AR | Repayment of debt under a writ of execution | |

| IN | Repaying the investment tax credit | |

| TL | Repayment by the founder (participant) of the debtor organization, the owner of the property of the debtor - a unitary enterprise or a third party of debt during bankruptcy | |

| RK | Repayment by the debtor of debt included in the register of creditors' claims during bankruptcy | |

| ST | Repayment of current debts during the specified procedures | |

| Tax period and document number | ||

| Field value 106 “Basis of payment” | The value that must be indicated in field 107 “Tax period indicator” | The value that must be specified in field 108 “Document number” |

| When filling out the field, do not put the “No” sign | ||

| TP, ZD | See table below | 0 |

| TR | The payment deadline established in the request for payment of taxes (fees). Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Number of the request for payment of taxes (insurance premium, fees) |

| RS | The date of payment of a portion of the installment tax amount in accordance with the established installment schedule. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Installment decision number |

| FROM | Deferment end date. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Postponement decision number |

| RT | The date of payment of part of the restructured debt in accordance with the restructuring schedule. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Restructuring decision number |

| PB | The date of completion of the procedure used in the bankruptcy case. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | |

| ETC | The date on which the suspension of collection ends. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Number of the decision to suspend collection |

| IN | Date of payment of part of the investment tax credit. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Number of the decision on granting an investment tax credit |

| VU | External management completion date. Enter the data in the format “DD.MM.YYYY” (for example, “04.09.2017”) | Number of the case or material considered by the arbitration court |

| AP | 0 | Inspection report number |

| AR | 0 | Number of the enforcement document and the enforcement proceedings initiated on the basis of it |

| 0 | 0 | 0 |

| Tax period, if the basis of payment is “TP, ZD” | ||

| Description | ||

| The first two digits of the indicator are intended to determine the frequency of payment of taxes (insurance premiums, fees) established by the legislation on taxes and fees | ||

| MS | Monthly payments | |

| HF | Quarterly payments | |

| GD | Annual payments | |

| In the 4th and 5th digits of the tax period indicator, enter the number: | ||

| from 01 to 12 | Month | |

| from 01 to 04 | Quarter | |

| 01 or 02 | Semester | |

| In the 3rd and 6th digits of the tax period indicator, put dots as dividing marks | ||

| The year for which the tax is transferred is indicated in 7–10 digits of the tax period indicator | ||

| When paying tax once a year, enter zeros in the 4th and 5th digits of the tax period indicator | ||

| If the annual payment provides for more than one deadline for paying the tax (fee) and specific dates for paying the tax (fee) are established for each deadline, then indicate these dates in the tax period indicator | ||

| For example, the payment frequency indicator is indicated as follows: | ||

| "MS.03.2017"; "KV.01.2017"; "PL.02.2017"; "GD.00.2017" | ||

| Date of payment basis document | ||

| Payment basis code (field 106) | What date is entered in field 109 | |

| TP | date of signing the tax return (calculation) | |

| ZD | «0» | |

| TR | date of the tax authority's request for payment of tax (insurance contribution, fee) | |

| RS | date of decision on installment plan | |

| FROM | date of decision to postpone | |

| RT | date of decision on restructuring | |

| PB | date of the arbitration court's decision to initiate bankruptcy proceedings | |

| ETC | date of decision to suspend collection | |

| AP | date of the decision to prosecute for committing a tax offense or to refuse to prosecute for committing a tax offense | |

| AR | date of the writ of execution and the enforcement proceedings initiated on its basis | |

| IN | date of decision to grant investment tax credit | |

| TL | date of the arbitration court ruling on the satisfaction of the statement of intention to repay the claims against the debtor | |

| Payment order | ||

| Field number | The value that the field takes | Reasons for writing off funds |

| 21 | 3 | When transferring taxes and mandatory insurance contributions (as well as penalties and fines for these payments), the values “3” and “5” can be indicated in field 21 “Payment order”. These values determine the order in which the bank will make payments if there are not enough funds in the organization's account. The value “3” is indicated in payment documents issued by tax inspectorates and branches of extra-budgetary funds during forced debt collection. The value “5” is indicated in payment documents that organizations draw up independently. Thus, other things being equal, orders from organizations to transfer current tax payments will be executed later than requests from regulatory agencies to pay off arrears. This follows from the provisions of paragraph 2 of Article 855 of the Civil Code of the Russian Federation and is confirmed by letter of the Ministry of Finance of Russia dated January 20, 2014 No. 02-03-11/1603 |

| 5 | ||

| Unique Payment Identifier (UPI) | ||

| Props number | Props value | |

| 22 | The “Code” field must contain a unique payment identifier (UPI). This is 20 or 25 characters. The UIP must be reflected in the payment order only if it is established by the recipient of the funds. The values of the UIP must also be communicated to payers by recipients of funds. This is stated in paragraph 1.1 of the Bank of Russia instruction dated July 15, 2013 No. 3025-U. | |

| When paying current taxes, fees, insurance premiums calculated by payers independently, additional identification of payments is not required - the identifiers are KBK, INN, KPP and other details of payment orders. In these cases, it is enough to indicate the value “0” in the “Code” field. Banks are obliged to execute such orders and do not have the right to require filling out the “Code” field if the payer’s TIN is indicated (letter of the Federal Tax Service of Russia dated April 8, 2016 No. ZN-4-1/6133). | ||

| If the payment of taxes, fees, and insurance premiums is made at the request of regulatory agencies, the value of the UIP must be indicated directly in the request issued to the payer. Similar explanations are contained on the official website of the Federal Tax Service of Russia and in the letter of the Federal Tax Service of Russia dated February 21, 2014 No. 17-03-11/14–2337 | ||

Based on materials from: taxpravo.ru, buhguru.com

In the current domestic system of non-cash payments, it is difficult to overestimate the role of the payment order. However, difficulties often arise with filling out certain fields of this form, which in turn can lead to problems with processing and crediting the payment. To simplify the procedure for generating a document, you can use the link to view a sample of the fields for a payment order in 2017.

Payment order

The official payment order form was approved by the Central Bank of Russia in Regulations dated June 19, 2012 N 383-P. You can download it, including using the Consultant Plus legal reference system.

In addition to the form itself, the Central Bank of Russia in the same Explanations developed and described the fields of the payment order.

Before you start filling out the order form, you should study the requirements for the content of its sections set out in Appendix No. 1 to the Central Bank's Explanations. You also need to remember the recommendations of the Russian Ministry of Finance about the need to fill out all the fields used to identify the transfer.

Appendix No. 3 to the above act of the Central Bank of Russia contains the payment order form with field numbers.

It should be noted that the Central Bank of Russia assigned a specific code to each section and payment details, and also described the requirements for its content.

The abbreviated notation looks like this:

- “1” is used to indicate the title of the document;

- “2”—form code according to OKUD;

- “3” — serial number;

- “4” - the day, month and year of its compilation;

- “5”—payment order column for the type of payment;

- “6” - the amount stated in words;

- section “7” is intended to reflect the result in digital terms;

- field “8” reflects the name or full name of the payment originator;

- “9” is an indication of his account;

- “10” serves to reflect the payer’s bank;

- “11” and “12” - for the BIC and the account of the above-mentioned credit institution;

- “13”—payment order field number—used to enter data about the bank of the transfer recipient;

- “14” and “15” are intended for entering a BIC and an account of such a structure;

- the name or full name of the recipient of the money is entered in section “16”, and his account number - in field “17”;

- the value “18” was entered to indicate the type of operation;

- to reflect information about the deadline, purpose and order of transfer, in 2017 the payment order field numbers from “19” to “21” are used;

- “22”, or the code in which the UIP or UIN is entered;

- the reserve field is displayed as “23”;

- the purpose of the payment should be recorded in column “24”;

- details “60” and “61” reflect the TIN of the parties to the money transfer transaction;

- fields “101” - “110” are used to record information when making transfers in favor of the budget;

- columns “43” and “44” are intended for the signature of the payment processor and his seal;

- “45” - bank notes on debiting money;

- the value “62” is used to indicate the date of receipt of the order by the credit institution;

- completing the description of the fields of the payment order, it should be noted that column “71” indicates the date of debiting the funds from the account.

When making payments to the budget system, the following fields must also be completed:

- section “101” is intended to indicate the status of the payment originator;

- columns “102” and “103” are used to enter the checkpoints of the parties to the settlements;

- BCC is contained in field “104”;

- a familiar place with the code “105” is used to display OKTMO;

- section “106” is intended to record the basis for payment, and the number and date of such a document are indicated respectively in details “108” and “109”;

- the tax period is displayed in column “107”;

- subsection “110” is not currently issued.

In conclusion, we provide a sample payment order with fields for 2017 for your reference. It is available here.

sample payment order with field numbers