You can claim VAT for deduction in parts in different periods on the same invoice. Now this has been officially recognized by the officials themselves. What influenced the change in their position and how to apply the deduction in several stages in practice, we will tell you in more detail in our article.

Previously, the Tax Code did not contain any instructions regarding the “spread” of VAT deductions across different tax periods, so officials, guided by the principle “what is not permitted, is prohibited,” concluded that applying the deduction in parts is unlawful (Articles 171, 172 of the Tax Code of the Russian Federation) . Similar explanations could be seen repeatedly in letters from the Ministry of Finance of Russia (letters from the Ministry of Finance of Russia dated December 9, 2010 No. 03-07-11/483, dated October 13, 2010 No. 03-07-11/408, dated January 16, 2009 No. 03-07-11 /09).

Meanwhile, almost all courts considered it possible to apply a deduction on one invoice in several stages (regulatory Federal Antimonopoly Service of the Moscow Region dated 02.12.2013 No. F05-15985/12, dated 03.31.2011 No. F05-609/11, dated 03.25.2011 No. KA -A40/1116-11, FAS SKO dated 03/17/2011 No. A32-16460/2010, FAS PO dated 10/13/2011 No. F06-8602/11). The arbitrators noted that such use of deductions does not contradict the norms of the Tax Code and does not lead to non-payment of tax to the budget. The main thing is that parts of the deduction for one invoice must be declared within a three-year period (paragraphs 27, 28 of the post of the Plenum of the Supreme Arbitration Court of the Russian Federation dated May 30, 2014 No. 33).

Part of the VAT deduction can be transferred to the following periods

From January 1, 2015, significant changes were made to Article 172 of the Tax Code. According to the amendments, the taxpayer has the right to claim VAT deductions (clause 2 of Article 171, clause 1.1 of Article 172 of the Tax Code of the Russian Federation) in tax periods within three years after goods are registered. This means that companies can now “play” with deductions and claim them whenever it suits them. For example, in order to prevent the VAT amount from arising for reimbursement, part of the deduction can now be quite easily transferred to the following periods. In this way, the company will avoid a thorough desk audit, because when indicating the amount of VAT to be reimbursed in the declaration, tax authorities during a desk audit require the submission of all documents justifying the right to deduction. And not all accountants want to deal with this.Of course, the new norm of the Tax Code does not contain clear permission to apply VAT deductions in parts, but it is clear that since the possibilities for deductions have expanded, there is now no point for tax authorities to prohibit splitting the deduction. And, fortunately for the companies, the corresponding explanations from officials were not slow to appear.

Thus, recent letters from the financial department (letters from the Ministry of Finance of Russia dated 04/09/2015 No. 03-07-11/20290, 03-07-11/20293) say that the amount of “input” VAT on one invoice can be declared to deduction in parts in different tax periods. However, it should be noted that this permit does not apply to VAT on acquired fixed assets, equipment for installation and intangible assets, since in respect of them the tax is deductible in full (clause 1 of Article 172 of the Tax Code of the Russian Federation). Also, this rule does not apply to other deductions of VAT (for example, calculated from amounts of payment, advance payment; presented by the seller of goods (works, services) in relation to amounts of payment, partial payment; paid as a tax agent, etc.). Such deductions should be made in the tax period in which the taxpayer meets the relevant conditions.

Algorithm of actions for accepting VAT deduction in parts

The company received an invoice from the supplier, on which it wants to deduct VAT in parts. As for the postings, first the full amount of VAT indicated in this invoice is reflected in the debit of account 19. Next, the accountant determines what part of this amount he wants to deduct in the current tax period. And for the same amount, this invoice is registered in the purchase book.Similar actions should be carried out in the next quarter, until the quarter until the entire deduction for this invoice is “spent”. Thus, the same invoice, but only for different amounts, will appear in the purchase book more than once. If you add up all these amounts, the accountant should “come out” with the amount indicated on the invoice itself.

PJSC "Volna" in April 2015 purchased a car from LLC "Moscow Auto Sales Salon" for the purpose of its further sale for a total amount of RUB 1,416,000. (including VAT - 216,000 rubles). The accountant of Volna PJSC decided to “scatter” the deduction in equal parts over three quarters (II, III and IV quarters of 2015).

In April 2015 (Q2), the following entries should be made in accounting when purchasing a car:

DEBIT 08 CREDIT 60

RUB 1,200,000 - the cost of the car is reflected;

DEBIT 19 CREDIT 60

216,000 rub. - reflects the amount of “input” VAT;

DEBIT 68 CREDIT 19

72,000 rub. (RUB 216,000: 3) - the first part of the VAT deduction is reflected.

For the same amount, the accountant of Volna PJSC should register an invoice from Moscow Auto Sales Salon LLC in the purchase book for the second quarter of 2015.

The accountant will have to make the last entry and the last action in the third and fourth quarters of 2015.

The question arises: when exactly to include subsequent parts of VAT in the purchase book? It doesn't really matter. Can be turned on any day of the quarter. But, in our opinion, it is most convenient to register the deduction in the purchase book on the first working day of the quarter. And it is advisable to consolidate this procedure in the order on the accounting policy of the organization.

In practice, the following question may arise. When starting to use the VAT deduction on one invoice, is it possible to transfer the other part of the VAT deduction not to the next nearest quarter, but to “jump” over a quarter or even quarters? Companies that, for some reason, did not have sales operations in a certain quarter (for example, companies with a seasonal nature) may want to do this. In our opinion, this can be done. The main thing is to ensure that all parts of the deduction are claimed within the three-year period.

Cross-reconciliation with the Federal Tax Service

Since 2015, companies have been reporting VAT using a new form and new rules. The main change is that the declaration form has now been expanded and includes sections in which data from the taxpayer’s purchase and sales books are indicated. Upon receipt of the declaration, the tax authorities perform a quarterly cross-reconciliation of all invoices indicated in the reporting between sellers and buyers. In the information from the supplier's sales book there must be an entry that corresponds to an entry in the information from the buyer's purchase book. All this will be done using information systems.If the buyer, having decided to take advantage of the possibility of applying a deduction in several steps, reflects the supplier’s invoice not for the full amount, but for a part of it, then it is obvious that a discrepancy will arise during reconciliation in the tax office. Could there be negative consequences for the supplier or buyer in this case?

No, there will be no negative consequences. Yes, the company may encounter some inconveniences in the form of receiving a request from the inspectorate to provide explanations and documents. Indeed, if the information contained in the supplier’s declaration does not correspond to the buyer’s information, if these discrepancies indicate an underestimation of the amount of VAT or an overestimation of the tax claimed for reimbursement, tax authorities have the right to request invoices, primary and other documents related to these transactions (clause 8.1 Article 88 of the Tax Code of the Russian Federation). But in this case, both parties do not violate anything; the buyer’s application of the deduction in parts is legal, which means that the buyer will be able to give comprehensive explanations and submit the necessary documents.

Opinion

Marina Kosulnikova, chief accountant of the Galan companyIt’s safe to split the deduction

Since 2015, tax deductions for VAT can be claimed within three years after the registration of goods (work, services), property rights or goods imported into the territory of the Russian Federation and other territories under its jurisdiction (p 1.1 Article 172 of the Tax Code of the Russian Federation).

Let us note that the legislation does not contain any restrictions on the choice of the period in which the amount of VAT on an invoice can be included in deductions. There is also no prohibition on deducting part of the tax on an invoice (split into several periods) (regulatory Federal Antimonopoly Service of the Moscow Region dated February 12, 2013 No. F05-15985/12). So the deduction can be claimed on the basis of one invoice in parts in different tax periods within a three-year period (letters of the Ministry of Finance of Russia dated 05/18/2015 No. 03-07-RZ/28263, dated 04/09/2015 No. 03-07-11/20293 ).

This innovation allowed accountants to distribute deductions at their own discretion, for example, to avoid tax audits, when a large share of deductions (more than 89%) increases the likelihood of an on-site audit (clause 3 of Appendix No. 2 to the order of the Federal Tax Service of Russia dated May 30, 2007 No. MM-3 -06/333@) or the refundable tax leads to a desk audit (clause 8 of Article 88 of the Tax Code of the Russian Federation).

However, not all accountants have yet adapted to the innovations; many are stopped by the fear of having to explain themselves to inspectors. Indeed, from this year, the VAT return includes information from the books of purchases and sales (in some cases, information is taken from the journal of received and issued invoices) (clause 5.1 of Article 174 of the Tax Code of the Russian Federation). As a result, tax authorities can automatically compare information about the transactions of counterparties. Discrepancies in data with the counterparty may result in additional taxes, penalties and fines.

We believe that splitting the deduction for one invoice into several quarters (within a three-year period) should not cause any problems for the buyer and seller. After all, a record of a received invoice in the purchase book only means that someone has already reflected this invoice in the sales book and uploaded this information to the tax database. The main thing is that the amount claimed for deduction on the invoice is equal to or less than the tax in this invoice issued by the seller.

From a purely technical point of view, breaking down the deduction by invoice should also not pose any difficulties. The purchase ledger should reflect only that part of the input VAT for which deductions are made in a given period. It turns out that one invoice will be indicated in the purchase book as many times as the number of parts the deduction will be divided into.

2016-12-08T13:45:26+00:00With this article I open a series of lessons on working with VAT in 1C: Accounting 8.3 (revision 3.0). We will look at simple examples of accounting in practice.

Most of the material will be designed for beginner accountants, but experienced ones will also find something for themselves. In order not to miss the release of new lessons, subscribe to the newsletter.

Let me remind you that this is a lesson, so you can safely repeat my steps in your database (preferably a copy or a training one).

So let's get started

In the middle of the last century Laura Maurice(French) invented a new tax - Value added tax, abbreviated.

The idea of the tax turned out to be so successful that over time, VAT appeared in other countries (now there are 137 of them); VAT came to Russia on January 1, 1992.

By the way, wonderfully structured information about VAT is on the tax service website, I recommend reading it (link).

Situation to consider

We (VAT payer)

01.01.2016 bought chair behind 11800 rubles (including VAT 1800 rubles)

05.01.2016 sold chair behind 25000 rubles (including VAT 3813.56 rubles)

Required:

- enter documents into the database

- create a shopping book

- create a sales book

- fill out the VAT return for the 1st quarter of 2016

We will do all this together and along the way I will draw your attention to the details that you need to know in order to understand the behavior of the program.

We make a purchase

Go to the “Purchases” section, “Receipts” item ():

We create a new document for receipt of goods and services:

We fill it out in accordance with our data:

When creating a new product item, do not forget to indicate the VAT rate of 18% in its card:

This is necessary for convenience - it will be automatically inserted into all documents.

We also pay attention to the “VAT on top” item highlighted in the document picture:

When you click on it, a dialog appears in which we can specify the method of calculating VAT in the document (on top or in total):

Here we can check the box “Include VAT in price” if you want to make input VAT part of the cost (attributed to 41 accounts instead of 19).

We leave everything as default (as in the picture).

We post the document and look at the resulting transactions (DtKt button):

Everything is logical:

- 10,000 rubles went to cost (debit 41 accounts) in correspondence with our debt to the supplier (credit 60).

- 1,800 rubles were spent on the so-called “input” VAT, which we will accept for offset (debit 19) in correspondence with our debt to the supplier (credit 60).

Total, after these postings:

- Cost of goods (debit 41) - 10,000 rubles.

- Input VAT to be credited (debit 19) - 1,800 rubles.

- Our debt to the supplier (credit 60) is 11,800 rubles.

This seems to be all, since often accountants, out of habit, pay attention only to the bookmark with accounting entries.

But I want to tell you right away that for the “troika” (as well as for the “two”) this approach cannot be considered sufficient. And that's why.

1C: Accounting 3.0, in addition to accounting entries, also makes entries in so-called registers. It is on the entries in these registers that she focuses her work.

The book of income and expenses, the book of purchases and sales, certificates, declarations for reporting... almost everything (except perhaps for such reports as Account Analysis, SALT, etc.), she fills out precisely on the basis of registers, and not at all accounting accounts .

Therefore, it is simply vital for us to gradually learn to “see” movements in these registers in order to better understand and, when necessary, correct the behavior of the program.So, let's go to the register tab " VAT Presented":

Income from this register accumulates our incoming VAT (similar to debit entry in account 19).

Let's check - have we met all the conditions for this receipt to be reflected in the purchase book?

To do this, go to the “Reports” section and select the “Purchase Book” item:

We form it for the 1st quarter of 2016:

And we see that it is completely empty.

The whole point is that we did not register the invoice received from the supplier. Let's do this, and at the same time let's take a look at what movements she makes through the registers (along with postings).

To do this, we return to the receipt document and fill in the number and date of the invoice from the supplier at the bottom of it, then click the “Register” button:

Please note the checkbox “Reflect VAT deduction in the purchase ledger by date of receipt.” This is the checkbox that is responsible for the appearance of our receipt in the purchase book:

Let's look at the postings and movements according to the registers of the received invoice (DtKt button):

The postings are quite expected:

- We subtract input VAT from account credit 19 to debit 68.02. With this operation we reduce our own VAT payable.

Total after this operation:

- As of March 19, the balance is 0.

- According to 68.02 - debit balance 1800 (the state owes us at the moment).

And now the most interesting thing, let’s look at the registers (over time you need to learn them all, along with the chart of accounts).

Register" VAT presented" - our old friend:

Only this time the entry was made as an expense. By doing this, we deducted the incoming VAT, similar to the credit entry for account 19.

And here is a new register for us" VAT Purchases":

You probably already guessed that it is the entry in this register that is responsible for getting into the purchase book.

Book of purchases

We are trying to re-form the purchase book for the 1st quarter:

And voila! Our receipt was included in this book and all thanks to the entry in the “VAT Purchases” register.

About the invoice journal

By the way, we did not consider the third register “Invoice Journal”. A record has been made on it, but let’s try to create this very log.

To do this, go to the “Reports” section, “Invoice Journal” item:

We create this log for the 1st quarter of 2016 and... we see that the log is empty.

Why? After all, we have entered the invoice and the entry has been made in the register. And the whole point is that since 2015, a log of received and issued invoices is kept only when carrying out business activities in the interests of another person on the basis of intermediary agreements (for example, commission trading).

Our invoice does not fall under this definition, and therefore it does not appear in the magazine.

Making the implementation

Go to the “Sales” section, “Sales (acts, invoices”) item:

We create a document for the sale of goods and services:

Fill it out in accordance with the task:

And again, we immediately pay attention to the highlighted item “VAT in total”.

We post the document and look at the postings and movements according to the registers (DtKt button):

Expected accounting entries:

- We wrote off the cost of the chair (10,000 rubles) as credit 41 and immediately reflected it as debit 90.02 (cost of sales).

- We reflected the revenue (25,000 rubles) on credit 90.01 and immediately reflected the buyer’s debt to us as debit 62.

- Finally, we reflected our VAT debt in the amount of 3813 rubles 56 kopecks to the state under credit 68.02 in correspondence with debit 90.03 (value added tax).

And if we now look at the analysis of 68.02, we will see:

- 1,800 rubles by debit is our input VAT (from the receipt of goods).

- 3,813 rubles and 56 kopecks on the loan is our output VAT (from sales of goods).

- Well, the credit balance of 2013 rubles and 56 kopecks is the amount that we will have to transfer to the budget for the 1st quarter of 2016.

Everything is clear with the wiring. Let's move on to registers.

Register" VAT Sales" is completely similar to the "VAT Purchases" register, with the only difference being that recording in it ensures that sales are included in the sales book:

Let's check it out.

Sales book

Go to the "Reports" section, "Sales Book" item:

We form it for the 1st quarter of 2016 and see our implementation:

Amazing.

The next stage on the way to creating a VAT return.

Analysis of VAT accounting

Go to the "Reports" section, "VAT Accounting Analysis" item:

We form it for the 1st quarter and very clearly see all charges (outgoing VAT) and deductions (input VAT):

VAT for payment is immediately displayed. All meanings can be deciphered.

For example, let's double-click the left mouse button on the implementation:

The report has opened...

In which, by the way, we see our mistake - we forgot to issue an invoice for sale.

Let's fix this bug. To do this, go to the implementation document and at the very bottom click the “Write an invoice” button:

VAT Accounting Assistant

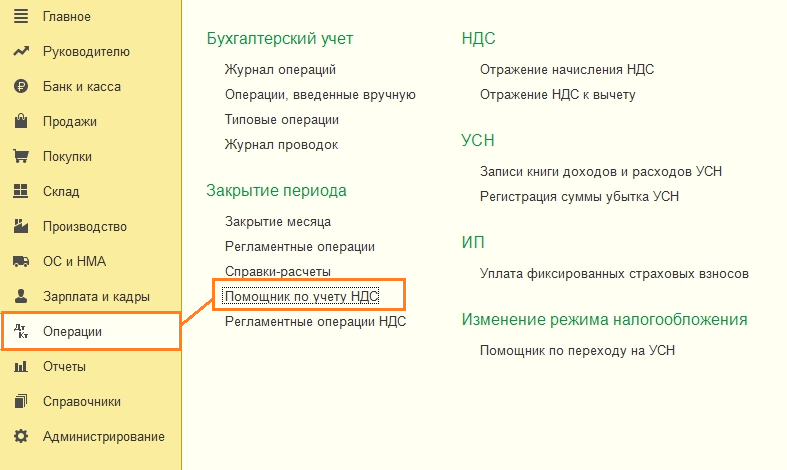

Now go to the “Operations” section and select “VAT Accounting Assistant”:

We form it for the 1st quarter of 2016:

Here, in order, we talk about the steps that need to be completed to generate a correct VAT return.

First, let’s transfer the documents for each month:

This is necessary in case we entered documents retroactively.

We skip creating purchase book entries, because for our simplest case they simply won’t be there.

And finally, click on the item “VAT Return”.

Declaration

The declaration has opened.

There are many sections here. We will consider only the main points.

First of all, in Section 1 the final amount to be paid to the budget was filled in:

Section 3 provides the tax calculation itself (outgoing and incoming VAT).

It is advisable to structure modern document flow with programs that allow you to personalize reporting in detail, reform, and carry out operations without resorting to the traditional nomenclature of affairs. A complex issue is solved through a common application.

Beginning of work

The reform of the value added tax is documented in Appendix 1C 8.3 Accounting 3.0 VAT accounting with accounting registers, where you can find entries in the Books of sales, purchases, accounting reports Dt 19 Kt 68. Input VAT accepted for deduction with the restored amount is documented in the above Sales Book with the participation of invoices - input VAT. Personalization reflecting the restoration is indicated in the Operations/Routine VAT operations/create/restoration interface.

The beginning of value added tax recovery is determined from the entry, program operation. When a product is purchased or written off, you need to open the application, select a supplier, an invoice through the active “Add” tab. Next, you need to identify the actual document and attach it to the list - fill in the details. The specified value (amount) is not a VAT refund in 1C 8.3 Accounting 3.0, but for reform it must be registered using, for example, a Write-off Act.

Filling out analog lists

When it is impossible to identify an invoice (there are objective reasons), it is possible to determine adjustments based on the use of an accounting certificate, which indicates the amount of VAT, and further filling out the Sales Book. You can generate the necessary postings for different types of documents, when the recording of current information is carried out in an identical way. If the program is intensively used by an accountant, the list of document flows is quite large.

If non-productive real estate is built or acquired, the identification of value added tax is carried out in a similar way. The specifics of entering information are no different. Restoration and verification of VAT in 1C 8.3 Accounting 3.0 is possible from advances issued. If the tax was submitted for deduction earlier, the invoice is reformed according to advances. The deduction can be obtained using the payment amount invoice. Reformation of amounts: supplier, buyer is carried out upon shipment. If filled out incorrectly, errors can always be corrected.

In this article we will talk about the restoration of VAT and the reflection of this operation in 1C 8.3 using the example of the 1C Enterprise Accounting configuration.

Often the term itself "VAT restoration" raises questions. Let's try to explain it. In short, then recovery is the inverse operation receiving a deduction according to VAT, i.e. an adjustment is made based on the deduction already received, reducing this deduction or completely canceling it. If it makes more sense to someone, then theoretically we can say that we will reverse the VAT deduction completely or partially, depending on the situation. But that's just the term "reverse" in this case does not apply, but they say that “VAT must be restored.”

In more detail, upon receipt of materials, goods, fixed assets, etc. Input VAT is often a tax deduction that reduces the amount of tax payable at the time of receipt. In order to apply such a deduction, several conditions must match, for example:

- Correctly executed SF;

- The received values are used in activities subject to VAT;

- The recipient of the valuables is a VAT payer, etc.

Now let’s imagine a situation where, at the time of capitalization of the assets, all these conditions were met, and the deduction was accepted. After some time, the conditions changed, and it turned out that the deduction could not be used. This is where VAT is restored.

Another option when it is necessary to restore VAT is prepayment to the supplier by the buyer. By making an advance payment, the buyer can use a VAT deduction by creating an accounting entry 68.VAT - 76.VA. When the buyer receives the shipment for such an advance, he will make a deduction for the received items with posting 68.VAT - 19. Then it turns out that there will be two deductions for one shipment. This situation is impossible, so the first deduction must be restored.

The list of situations when VAT should be restored is given in the Tax Code, Art. 170 clause 3. And although the practice of court decisions suggests that this list is closed, nevertheless, tax authorities often require the restoration of VAT in other cases, for example, in case of theft of property. Here the enterprise itself must decide whether to restore the tax or not (in this case, court hearings will be necessary).

Since the restoration of VAT always leads to an increase in the amount of tax payable, in the transactions Kt there will always be 68.VAT, and for Dt options are possible, depending on the situation. Such transactions should be reflected in Book of Purchases.

Let's look at the most common cases of VAT recovery.

VAT recovery using the example of 1C: Accounting configuration

Now from theory to practice. Let's consider two options for how to reflect the restoration of VAT in 1C Accounting.

Example 1. The most common case of VAT recovery. The buyer made an advance payment for the consignment of goods, both counterparties are VAT payers. The prepayment amount is 118,000 rubles, incl. VAT 18,000. A few days after the prepayment, the organization received material assets in the amount of 94,400 rubles, incl. VAT 14,400 rub.

Accounting for advance payments in 1C is well automated. The correct transactions were automatically generated for payment.

If at this moment we form Shopping book we will have two deductions for one delivery.

VAT should be restored. To do this in the menu Operations select an item

Offers to repost documents and create routine operations - creating purchase and sales ledger entries.

We are interested in Click the button Complete the document, the tabular part will be generated automatically.

Let's look at the wiring. The program automatically recovers VAT by analyzing the advance amount and subsequent shipments. In our case, the delivery is less than the advance payments paid, we restore the amount in an amount equal to the shipment received from the supplier.

Example 2. In the 4th quarter, on the received batch of materials from example 1, VAT should be restored from the amount of 40,000 rubles, the estimated amount of VAT is 7,200 rubles.

In this case, the program cannot automatically determine in what period and volume the VAT should be restored. Therefore, we create a corresponding document VAT restoration. It is in the section

Press the button Create, From the list of options, select a document for VAT restoration.

To prevent VAT from getting stuck on account 19, it must be written off. A document can be created based on receipt.

By default, the entire receipt amount is offered for adjustment; we should adjust it.

On the bookmark Write-off account indicate the account 91.02.

Please note the meaning of the expense guide. Here you can set the parameter whether expenses are accepted as expenses for the purpose of calculating income tax or not.

If accepted, the postings will be as follows:

Another common example that many businesses may encounter is a change in the supply amount due to an adjustment in price and/or quantity of items shipped, which may result in the need to recover VAT. Such operations lead to the appearance of adjustment invoices, the procedure for reflecting which we will discuss in detail in another article.

Some government agencies carry out profit-generating activities. If the general taxation system is applied, the institution's accountant is familiar with the deduction of input VAT. We can say that tax accounting is one of the most complex sections of accounting, but there is still very little information about its management in 1C programs for the public sector. In this article I would like to talk about the deduction of value added tax using the example of purchasing an operating system in the program “1C: Public Institution Accounting 8, edition 2.0”.

Let me start with the fact that a tax deduction is a way to reduce the amount of VAT that an institution pays to the budget. This means that such a deduction is strictly regulated by the Tax Code of the Russian Federation.

In particular, when purchasing a fixed asset by a state-owned institution, it is possible to deduct VAT only if this fixed asset will subsequently be used in activities that bring profit to the institution. Another condition is the availability of primary documents drawn up in accordance with all the requirements of the Tax Code.

There is also a small list of exceptions under which VAT is not deductible, even if the two above conditions are met:

- the fixed asset was acquired by institutions that are exempt from paying tax or that are not taxpayers;

- if the work, services or goods performed are sold (sold) outside the territory of the Russian Federation;

- if the work, services or goods performed are not sold, that is, no profit is received in the tax period.

We've sorted out the conditions, now let's start reflecting the example in 1C: BGU. We purchased a fixed asset that will participate in income-generating activities.

To make a purchase, we use the document “Purchase of OS, intangible assets, legal acts” already known to us:

We create a document and fill in the necessary data:

By default, when entering a document, the VAT amount is not included in the total cost of the purchased fixed asset (VAT is added on top). To change the settings and accept VAT for accounting, use the special link in the header of the document:

A special form opens:

There are two flags in this form. To include the VAT amount in the price, set the flag in the first line. To deduct VAT - in the second line:

After clicking the OK button, the document table is modified:

Firstly, the VAT amount is included in the total cost of the acquired fixed asset, and secondly, a new flag appears - “Distributed”. This flag is set if the fixed asset will participate in activities both subject to and exempt from VAT. In our example, the entire amount will be deducted; the flag is not set.

Next, fill in the tabs sequentially:

Let's review the document and check the wiring:

The first posting to the accounts of group 502.00 is the posting for accepting monetary obligations.

The second entry is the formation of a capital investment in a fixed asset.

A third posting also appears - this is where the VAT amount is allocated.

The fourth entry for tax accounting.

Let's go back to the third wiring. In order to understand what account is used in it, let’s turn to the Chart of Accounts. You can find it:

We find the account we are interested in:

As we can see, in the group of accounts 210.00 “Other settlements with debtors” there are two sections with accounts that relate to VAT calculations on acquired material assets.

Group 210.01 accounts were used until 2015.

In 2014, new accounts were introduced - group 210.10, which includes sub-accounts 210.11 and 210.12. In accordance with the order of the Ministry of Finance, the lines of group 210.01 must be excluded from the Chart of Accounts. But in the program “1C: Public Institution Accounting 8, edition 2.0” these accounts were left to reflect the turnover of previous periods on these accounts. Therefore, in transactions created after 2015, accounts of group 210.12 are used.

I would also like to note that subaccounts 210.Р1, 210.Н1, 210.Р2, 210.Н2 are special accounts of the 1C: BGU program. That is, they are absent from Order 157n, which regulates the composition of the Chart of Accounts. These sub-accounts were introduced by 1C for separate VAT accounting for taxable and non-VAT-taxable transactions.

There is some controversy regarding this decision by 1C. On the one hand, adding subaccounts for clarification is a convenient solution that does not in any way contradict the legislation regarding accounting. On the other hand, in order to use these subaccounts, the institution must reflect this fact in its accounting policies. When approving an institution’s working chart of accounts, it is imperative to think through such points in advance.

In the standard posting, account 210.Р2 was used - “Calculations for VAT on purchased material assets, works, services”, since the entire amount of VAT was allocated.

After the document has been posted, it is necessary to reflect the received invoice in the program, which is the basis for applying the deduction. You can enter it directly from the document form:

The document is almost completely filled with the necessary data:

On the “Advanced” tab, you need to indicate the number and date of the primary document:

On the “Accounting transaction” tab, select a typical transaction:

Postings for this document are not generated at the time of posting. They will be created later by another document. This is due to the fact that the acceptance of fixed assets for accounting can be carried out later than its purchase, and we have the right to reflect the deduction of VAT only after the fixed asset has been accepted for accounting.

In our case, the fixed asset is taken into account immediately.

In this article I want to show a convenient mechanism for the input assistant based on: from the document “Receipt of fixed assets, intangible assets, legal acts” enter the document “Acceptance for accounting of fixed assets, intangible assets, legal acts”. Take into account the fact that the assistant is used if the initial cost of the purchased fixed asset did not include any other costs (delivery, assembly).

We find the receipt document we created:

Let's use a special button:

The assistant window opens:

Fill in the data and move through the tabs using the button:

After filling out, click the “Finish” button, the object is formed, and the assistant form closes. A minor inconvenience is that the generated document cannot be opened or posted. You need to find the document in the list:

After verification, we review the document and check the created movements on the accounts:

The acquired fixed asset was accepted for accounting and put into operation. In order to deduct the VAT allocated on a purchase, you need to create the document “Creating purchase ledger entries.”

This operation is usually performed at the end of the month and summarizes all VAT information for deduction for the period. This document includes all invoices for which tax has not yet been deducted. You can find it:

Create a document:

In the document form we will use a special button:

The table shows the invoice that we entered:

Let's check the book. operation and carry out the document:

Postings created by the document:

This document accepted for deduction the VAT presented by the supplier upon the acquisition of a fixed asset (in other words, the amount of tax payable in account 303.04 “Calculations for value added tax” was reduced.

If you have any questions, you can ask them in the comments to the article.